Five steps to help you achieve retirement balance

Are you ready to retire? How do you know if you’re ready? How do you get ready?

Now that you’re getting closer to retirement, you've got questions—and we've got answers. Following these five steps can help you get closer to achieving retirement balance.

1 Calculate your retirement spending needs

Picture your retirement

Knowing how you want to spend your time can help you figure out your retirement expenses.

Ask yourself:

- When do you want to retire?

- How does your retirement date affect your savings and spending?

- What will you do in your free time?

- Will you get a part-time job or start a second career?

- Where will you live?

With this picture in mind, you can then use the retirement planner1 at myplan.johnhancock.com or our mobile app to:

- Learn just how much money you may need for retirement

- See how your projected retirement expenses and income change over time

- Personalize and refine your projections for more accurate results

- Receive your retirement action plan to help you get or stay on track

To use the retirement planner, simply sign in to your retirement account and choose Let’s go on the homepage.

Look at your health insurance options

Before you leave your job, find out about options for health insurance—what’s offered through your company and what’s available through independent medical plans, Medicare, and Medicaid. Ask about monthly costs, deductibles, and limits, as well as the coverage for wellness visits, specialist visits, medications, and treatments.

Put together a budget

Some of your costs will stay the same, but some will be different. You’ll see in the retirement planner that when you retire, your spending is generally higher in the beginning—as you travel, eat out, and are generally active. Your spending then slows down for a bit, then goes up again, driven by healthcare expenses. Use the annual spending estimates in the retirement planner to help guide your budgeting.

Pay down your debt

Consider paying down your debt to help free up cash in retirement, including:

- Mortgages

- Car loans

- Credit cards

- Student loans

2 Map out your retirement income sources

So where does the money commonly come from to pay for your retirement? Most people rely on several different sources.

| You can use the retirement planner to calculate your projected retirement income. The amount is based on your Manulife John Hancock retirement account, estimated Social Security benefits, and any other sources you provide. |

3 Bridge the gap between spending and income

If there’s a difference between what you’re projected to have and what you’re projected to need, you’ll want to create a plan to help close the gap.

Consider small changes to help boost your savings

Review your contribution rate: If your retirement plan allows you to contribute, use the retirement planner to explore how different savings rates could help bring you closer to your savings goal. Even an increase as small as 1% can have a positive effect on your savings over time. And if you're age 50 or older, you can contribute an additional $7,500 to your retirement plan for a total of $31,000 in 2025. If you'll be 60, 61, 62, or 63 years old by the end of 2025, you can add even more—$11,250 instead of $7, 500—this year.

Adjust your spending: Check your budget to see if there are any expenses you can reduce or eliminate. For example, could you buy coffee three days a week instead of five? You can put any money you save toward your retirement.

Think about your investment strategy

The more your investments earn, the less money you might need to save for retirement, so make sure your investments are working for you. Consider putting some of your retirement savings in investments that have the potential to grow. How much you put in will depend on many things, including when you plan to retire. If you’re close to retiring, making your money last might be more important. Take the risk quiz to find out what kind of investor you are. The results can help you choose a mix of investments that balances potential risk and reward, helping you reach your goals.

These examples are for illustrative purposes only and are not indicative of any particular investment. There is no guarantee that any investment strategy will achieve its objectives. Neither asset allocation nor diversification guarantees a profit or protects against a loss. An asset allocation investment option may not be appropriate for all participants, particularly those interested in directing their own investments.

4 Make a plan to access your money in retirement

Understand the options for your retirement account

When you leave your employer, you generally have four choices for the money in your retirement plan. Before drawing down your savings to provide income in retirement, you should carefully review these options and choose the one that best fits your needs.2

YOUR OPTIONS |

OVERVIEW |

PROS |

CONS |

|---|---|---|---|

Keep your money where it is |

You may be able to keep your retirement money with your previous employer’s plan provider—check with the plan or employer to confirm. |

You can keep your current investment options, and you’ll continue to defer taxes. |

You can’t make new contributions, and you may need to repay plan loans, if you took any. |

Roll over to an IRA |

You can move your money to an IRA; it’s offered by many financial providers and not tied to an employer. |

You can make new contributions and add balances from other accounts, and you’ll continue to defer taxes. |

You can’t take a loan from an IRA, and a minimum account balance may apply. |

Roll over to a new employer’s plan |

You may be able to transfer your retirement account money to a new employer’s retirement plan—check with the plan to find out. |

You can make new contributions and may receive an employer match—plus, you'll continue to defer taxes. |

The investment choices and withdrawal options are set by the new plan. |

Take a cash distribution |

You can take your retirement plan money in cash—but be sure you know the pros and cons of doing so. |

You gain immediate access to your money (minus taxes and possible penalties). |

You’ll slow down progress on your retirement savings goal and you’ll likely owe taxes, plus a 10% IRS early withdrawal penalty, if you take the cash before turning age 59½. |

If you’d like help evaluating these options, call 888-695-4472 to speak with a Manulife John Hancock retirement consultant.3

Create a withdrawal—or drawdown—strategy

Your retirement could potentially last more than 30 years. Creating a drawdown strategy to manage how and when you’ll access your savings can help ensure your long-term financial well-being. Here are four common methods that help balance your need for income with the need to make your money last throughout your retirement.

Four potential drawdown strategies

1 Use our retirement planner Using the projections from our retirement planner at myplan.johnhancock.com, you can estimate how much you may need each year of your retirement for basics, healthcare, and nonessentials. It’s all done for you—and you can make adjustments if you’d like.¹ |

2 Earnings only Depending on your investments, you could choose to live on the income (interest and dividends) that your assets potentially generate. This allows you to continually pull income without eating into your principal. |

3 Systematic withdrawals With this method, you withdraw the same amount each year, adjusting the amount for inflation. You’ll need to estimate how long you expect your retirement to be and determine the percentage that you’ll be able to withdraw each year to make it last. One common method is to base your withdrawal percentage on the required minimum distribution (RMD) formula for rollover IRA or 401(k) savings. |

4 Time segmentation (bucket) method This method has you divide your retirement years and your assets into different segments, or buckets. Each investment bucket would correspond to a time period, generally with less risky investments (including fixed income and money market) funding the earlier years and risker assets (stocks) held for later years. This would also require that as you move through retirement and your buckets, you adjust the risk profile of future buckets as they draw closer to use. |

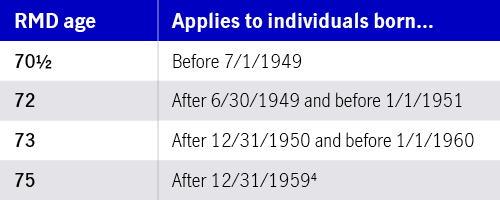

Factor in RMDs

Whichever strategy you choose, make sure it includes your RMDs—the amount you generally have to take out of your retirement account every year once you reach the age listed below.

Know what’s taxable and what’s not

The money you take out of your retirement account may be taxable, depending on the type of account you have.

Traditional 401(k) and IRA savings and earnings are generally taxed on distribution.

Qualified Roth 401(k) and IRA withdrawals may be tax free.5

Because the rules can be a bit tricky, you may want to contact a financial professional or tax accountant for help. You can use this retirement tax planning checklist to help jump-start the conversation.

5 Plan for the next phase

This step is all about getting things in order.

- Do you have a will that explains who should get your money and personal property after your death?

Without one, the courts will decide, and they may not make the same choices you would. Their decisions could lead to disagreement among your loved ones, causing undue stress and conflict.

- What about a living will and healthcare proxies that tell your loved ones what to do if you can’t speak for yourself?

When determining your wishes, think about what’s important to you, such as being independent, and what would affect your quality of life.

- Have you checked your beneficiary information lately?

Life events—marriage, divorce, the birth or adoption of a child, and the death of a loved one—can change who you want to receive your retirement savings. But just wanting someone to get your money isn’t enough. The beneficiary information on your retirement account is what matters.

Consider working with an estate attorney to create these documents and to help ensure you’re properly covered.

Retirement can be within reach. It’s time to get ready!

Important disclosures

Important disclosures

1 The projected retirement income estimates for your current John Hancock accounts, future contributions, employer contributions (if applicable), and other accounts set aside for retirement used in this calculator are hypothetical, for illustrative purposes only, and do not constitute investment advice. Results are not guaranteed and do not represent the current or future performance of any specific account or investment. Due to market fluctuations and other factors, it is possible that investment objectives may not be met. Investing involves risks, and past performance does not guarantee future results. 2 There are advantages and disadvantages to all distribution options; you are encouraged to review your options to determine if staying in a retirement plan, rolling over to an IRA, or another option is best for you. 3 John Hancock Personal Financial Services, LLC, is an SEC registered investment adviser. John Hancock Personal FInancial Services, LLC, 200 Berkeley Street, Boston, MA 02116. 4 Based on congressional intent and draft legislation to make a technical correction to Section 107 of SECURE 2.0. 5 Ordinary income taxes are due on withdrawal. Withdrawals before the age of 59½ may be subject to an early distribution penalty of 10%. Distributions from Roth accounts must be “qualified” for both the contributions and earnings to be treated as tax free. Certain conditions would apply. See your plan document for more details. All references to tax-free treatment of qualified distributions are intended to refer to the treatment of such distributions at the federal level only. You may want to consult a professional tax advisor regarding any tax issues discussed.

Clients should carefully consider a fund's investment objectives, risks, charges, and expenses before investing. To request a prospectus or summary prospectus with this and other important information, visit jhinvestments.com.

Mutual funds are distributed by John Hancock Investment Management Distributors LLC, member FINRA, SIPC.

MF3903764 4/25 MGR0331254364461

Related articles

What impact will Social Security have on your income?

Read more about what you can expect—and why