For complete information about a particular investment option, please read the fund prospectus or offering/trust document. You should carefully consider the objectives, risks, charges and expenses before investing. The prospectus or offering/trust document contains this and other important information about the investment option and investment company. Please read the prospectus or offering/trust document carefully before you invest or send money. Fund prospectus or offering/trust document may only be available in English.

Diversification does not guarantee a profit or eliminate the risk of a loss.

A target-date portfolio is an investment option comprising a fund of funds that allocates its investments among multiple asset classes that can include U.S. and foreign equity and fixed-income securities. The target date is the approximate date an investor plans to start withdrawing money. The portfolio’s ability to achieve its investment objective will depend largely on the ability of the subadvisor to select the appropriate mix of underlying funds and on the underlying funds’ ability to meet their investment objectives. The portfolio managers control security selection and asset allocation. There can be no assurance that either a fund or the underlying funds will achieve their investment objectives. Investors should examine the asset allocation of the fund to ensure it is consistent with their own risk tolerance. A fund is subject to the same risks as the underlying funds in which it invests. Because target-date funds are managed to specific retirement dates, investors may be taking on greater risk if the actual year of retirement differs dramatically from the original estimated date. Target-date funds generally shift to a more conservative investment mix over time. While this may help manage risk, it does not guarantee earnings growth. An investment in a target-date fund is not guaranteed, and you may experience losses, including principal value, at, or after, the target date. There is no guarantee that the fund will provide adequate income at and through retirement. Consider the investment objectives, risks, charges, and expenses of the fund carefully before investing. For a more complete description of these and other risks, please see the fund’s prospectus.

The glide path is the asset allocation within a target-date strategy that adjusts over time as participants' age increases and their time horizon to retirement shortens. The basis of the glide path is to reduce the portfolio's chance of loss as the participants' time horizon decreases. The asset mix of each portfolio is based on a target date, which is the expected year in which participants in a portfolio plan to retire and no longer make contributions. A team of asset allocation professionals adjusts each portfolio's investments over time to ensure a noticeable and steady shift from equities to fixed income in the years leading to retirement or during retirement, if applicable. Investors should examine the asset allocation of the portfolio to ensure it is consistent with their own risk tolerance. In developing the glide path, it was assumed that participants would make ongoing contributions during the years leading up to retirement and stop making those contributions when the target date is reached. The principal value of your investment, as well as your potential rate of return, is not guaranteed at any time, including at, or after, the target retirement date.

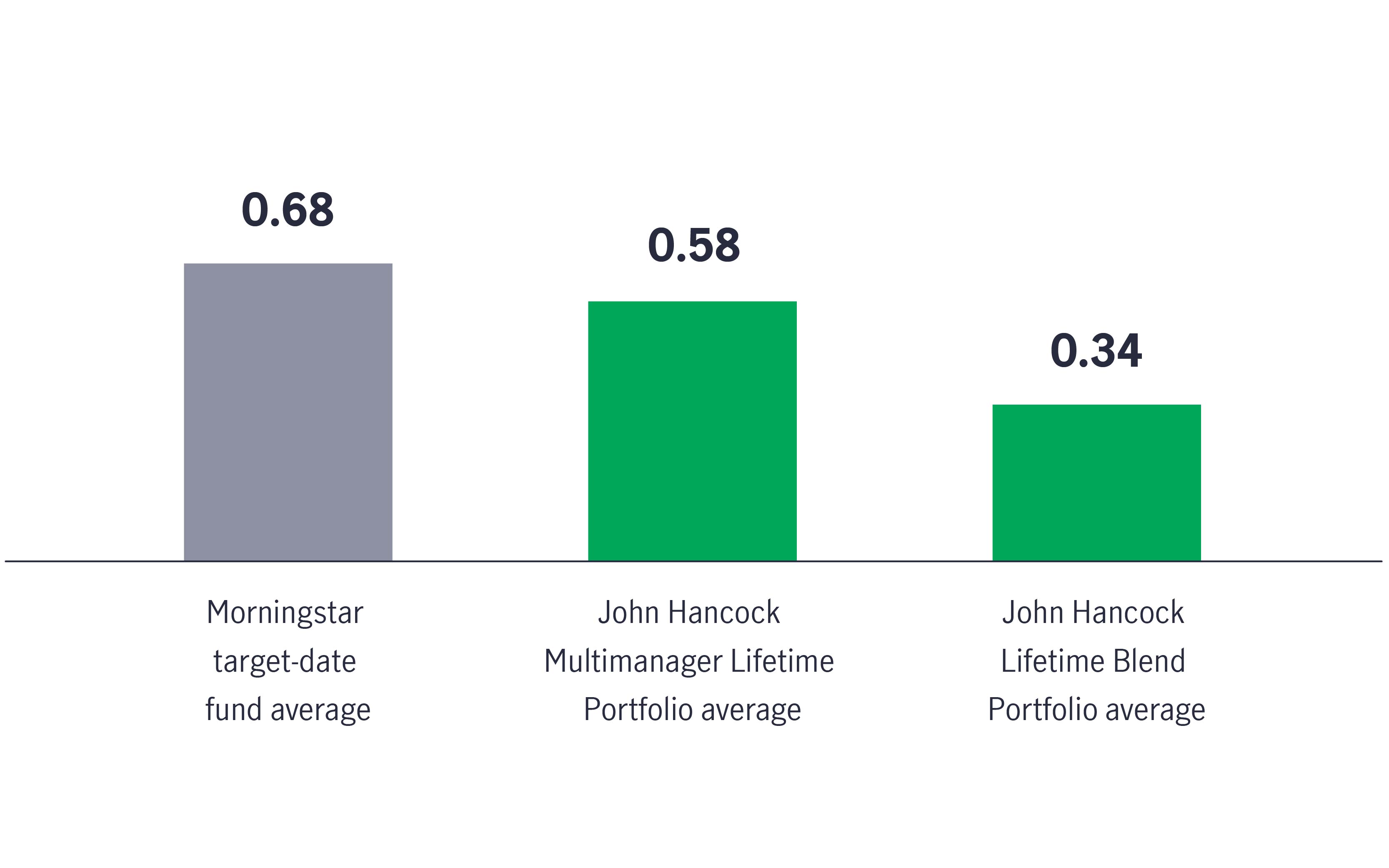

© 2024 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

John Hancock Retirement Plan Services LLC provides administrative and/or recordkeeping services to sponsors or administrators of retirement plans through an open-architecture platform. John Hancock Trust Company LLC, a New Hampshire non-depository trust company, provides trust and custodial services to such plans, offers an Individual Retirement Accounts product, and maintains specific Collective Investment Trusts. Group annuity contracts and recordkeeping agreements are issued by John Hancock Life Insurance Company (U.S.A.), Boston, MA (not licensed in NY), and John Hancock Life Insurance Company of New York, Valhalla, NY. Product features and availability may differ by state. All entities do business under certain instances using the John Hancock brand name. Each entity makes available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, each entity does not, and is not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity. Securities are offered through John Hancock Distributors LLC, member FINRA, SIPC.

John Hancock Investment Management Distributors LLC is the principal underwriter and wholesale distribution broker-dealer for the John Hancock mutual funds, member FINRA, SIPC.

NOT FDIC INSURED. MAY LOSE VALUE. NOT BANK GUARANTEED.

MF3081050