How a lot of the financial wellness buzz misses the point

Financial wellness is being discussed all over corporate America, among financial professionals, retirement plan sponsors, and recordkeepers. Unfortunately, the term can be ambiguous, with different meanings in different settings. In order to help people with financial wellness, an important step is defining what it means and then discussing its triggers to come up with solutions.

Financial wellness is about people

Financial wellness is a popular topic among plan sponsors and financial professionals these days. Financial services companies develop financial wellness programs that plan sponsors can offer their employees, so the term financial wellness gets used as if it’s a product. But it’s not a product, it’s about people and whether they’re financially well or not financially well—it’s a state of being. Just like healthcare benefits and blood pressure checks are meant to help people achieve physical wellness, retirement plans and budgeting tools are meant to help people achieve financial wellness.

At John Hancock, we spend a lot of time researching how to help people save for retirement and other life goals. Six years ago, we conducted our first financial stress survey, which confirmed what we had already guessed—that the lack of financial wellness was inhibiting retirement readiness and creating a lot of stress for people. Since then, we’ve continued to survey our participants to figure out how to help them achieve financial wellness on their way to retirement readiness, in part because 57% of participants told us they’d be more willing to save for retirement if they had help prioritizing all their financial concerns.

Poor financial habits hurt retirement readiness

When we ask people why they’re not saving more for retirement, their top two answers by far are poor spending habits and debt. This shows us the importance of financial wellness and its direct impact on saving for retirement.

The unfortunate exception to this is people with student loan debt, who say their student loans are their number one obstacle to saving for retirement. Among our participants with student loans surveyed this year, three-quarters had more than $20,000 in student loan debt at graduation, and 58% still do; 10% had $100,000 in loans at graduation, and the same amount still do. And it’s not only millennials with loans—it’s across generations. Forty-six percent of our participants younger than 36 have student loans, followed by 27% of participants aged 36 to 50, and 13% are aged 51 and older.

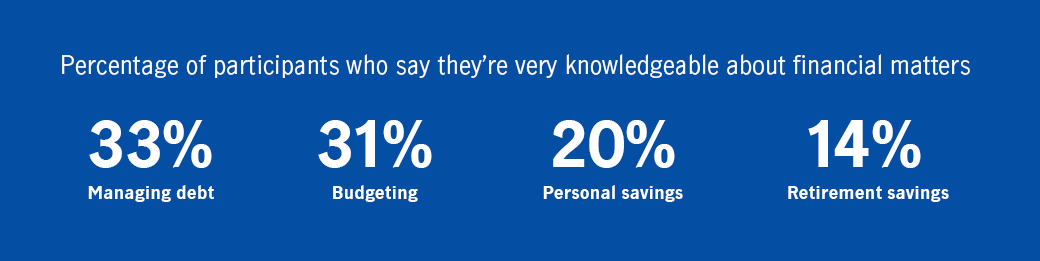

Lack of financial knowledge impedes financial wellness

The top financial worries, year after year, are saving enough for retirement and saving for emergencies. People know they should be saving, and they know they’re falling short. In the case of retirement savings, a quarter of participants say they’re willing to spend the time planning for retirement but don’t know how to start. This creates a great opportunity for financial representatives and plan providers to step in and provide the help participants are seeking.

Few people consider themselves very knowledgeable about basic financial concepts, and not only retirement savings. A third of participants say they know how to manage their debt, 31% know how to budget, 20% are comfortable with personal savings concepts, and only 14% are knowledgeable about retirement savings.

Financial wellness solutions have to get personal

We’ve also learned that, in order to help, we have to provide people with personally relevant solutions. A financial wellness profile is influenced by when and how people started their financial journey, who’s on the journey with them, the obstacles they experience along the way, their ultimate goals, and where they are today. According to our results, men have more saved for retirement than women, single people experience more financial stress than married people, millennials have more student loan debt than their parents and grandparents did, and Generation X is less prepared for retirement than Generation Z, millennials, and baby boomers. Financial wellness solutions have to reach people, wherever they are on their journey, and help them—whether it’s preparing for college, tracking their spending, saving for emergencies, or planning for retirement income.

When we talk about financial wellness, it’s important to remember that it’s a very human issue. It’s about each individual with his or her own financial needs today and each one's plan for retirement. It’s about helping people prioritize these goals to ease their stress about balancing competing priorities and reaching out to them with personally relevant tools and education to help them manage their complete financial picture.

It’s not just about increasing knowledge, it’s about improving their ability to help make good financial decisions and to take action toward achieving their goals. If we can help people achieve financial wellness, we can help enable them to be confident in their present financial situation, allowing them to achieve their retirement goals—and that’s healthy for all of us.

To see what else we learned about financial wellness in this year’s survey, please click here to view the results and download the full report.

Important disclosures

Important disclosures

John Hancock's sixth annual financial stress Survey, John Hancock, Greenwald & Associates, 2019. A survey of more than 3,500 workers to learn more about individual stress levels, their causes and effects, and strategies for relief.

MGS-P40695 GE 10/19 40695 MGR102419501945