Saving for college: do your homework

Being financially prepared to send your kids to college requires planning well before they take the SAT. Planning ahead and following some guidelines can help get your finances and your child’s education moving in the right direction.

How to get started with college savings

If you’re having a hard time figuring it all out and saving for college, you’re not alone. More than half of American households are saving for college,¹ and planning for college is a top worry among parents.² Yet fewer than one-third of parents say they have the knowledge needed to guide their children through the application and decision-making process.³

Here’s a six-step process to get you started.

1 Figure out the cost. Begin by calculating the expected cost of college. If you’re unsure, consider that the average annual in-state college tuition and fees totaled about $22,000 last year, average private tuition and fees were about $36,000, and more than 100 private colleges cost $50,000 or more.⁴

2 Consider your savings accounts. Identify how much of your current savings you can set aside for college, as well as how much you can set aside going forward. Then evaluate some of the tax-advantaged ways you can save for college, including:

a. 529 state prepaid tuition plans, which provide protection from rising college tuition costs by allowing you to lock in current costs. And for some, they offer tax benefits.

b. 529 education savings plans, which allow for tax-free distributions, considerable contribution limits, tax-advantaged growth, parental control, and contributions from people other than parents. They also offer a broad range of investment choices and the option to change beneficiaries.

While contribution limits for both types of 529 plans are high, they’re set on a state-by-state basis and may trigger gift taxes—see a tax or financial professional before proceeding.

c. Coverdell Education Savings Accounts (also known as education IRAs), which allow you to save with special tax treatment for the interest they earn.

A Roth IRA is a different type of account that also allows for tax-free distributions on higher education expenses. Again, you should speak with a financial professional to learn about rules for education expense withdrawals.

d. Education savings bonds, which are another option. The interest on Series EE and I federal savings bonds may be tax free if used for higher education expenses (subject to income limits).

3 Investigate aid. You may qualify for help based on family income. You should ask any college that your child’s considering about what types of financial aid it offers. The U.S. Department of Education’s Federal Student Aid (FSA) office also offers helpful resources, at https://studentaid.ed.gov/sa/fafsa.

4 Research scholarships and grants. The great thing about scholarships and grants is that they don’t need to be repaid, plus there are thousands available. Some are based on merit, some on background or affiliations (e.g., having a family member in the military), and others on financial need. There are many sources of scholarship information available, including the U.S. Department of Labor’s (DOL's) scholarship search tool, college financial aid offices, and high school guidance offices.

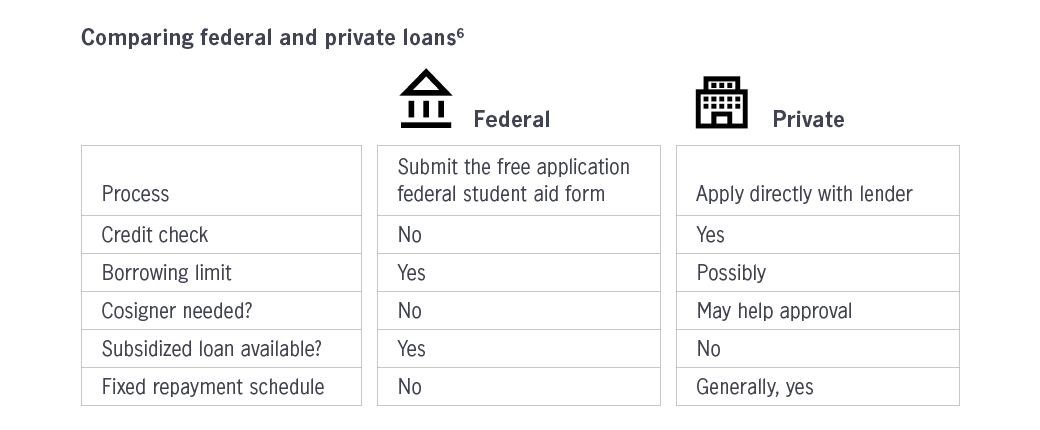

5 Explore student loans. There are many student loans available, both private and federal, with varying interest rates, repayment terms, and borrowing limits. While federal loans may be easier to obtain and generally offer more favorable terms, a limited number is granted each year. Many borrowers will need a combination of federal and private loans.

6 Consider other ways to make it more affordable. Some in-state schools offer tuition discounts to residents of neighboring states. Other ways of reducing tuition costs include taking extra classes while still in high school and at night or during the summer while in college, and joining the ROTC. Living at home can help you save on living expenses, and working part time can help pay some of the extra bills that come with college.

College prep isn't just for kids

Successfully saving and paying for college requires a plan. Once you figure out your goal and how you’re going to meet it, put your plan in motion.

Luckily, resources are available to help you plan. In addition to the FSA office and DOL, the College Board and many other organizations provide helpful tools and advice. Be sure to use a trusted resource. Many employers also provide access through offered benefits or a 401(k) service provider. Your kids don’t have to study for the SAT until they’re in high school—but the sooner you start doing your homework and putting a college savings plan together, the better.

1 “How America Saves for College,” Sallie Mae, 2018. 2 John Hancock's sixth annual financial stress survey. 3 “American Dream versus American Reality: How Parents Navigate and Influence their Kids’ Post-High School Education,” American Student Assistance, 2018. 4 “What you need to know about college tuition costs,” U.S. News and World Report, 9/19/18. 5 Federal Student Aid, an office of the U.S. Department of Education. 6 Sallie Mae, 2019.

Important disclosures

Important disclosures

The content of this document is for general information only and is believed to be accurate and reliable as of posting date, but may be subject to change. John Hancock does not provide investment, tax, or legal advice. Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

MGTS-P40529-GE 10/19 40529 MGR101119499936