What’s Social Security, and how much will I get when I retire?

Getting the most out of your Social Security benefit in retirement requires planning ahead. By understanding the factors that will go into the amount you'll receive, you'll have a better idea of what to expect at retirement.

How to make Social Security work for you

Social Security was set up to give retired workers a continuing source of income after retirement. Today, nearly 90% of Americans aged 65 or older count on that money to help them meet their expenses in retirement.1

But the average Social Security benefit is less than $18,000 per year,1 and that’s not even 40% of the median per capita income in the United States.2

Your Social Security benefit reflects payments you made to the program during your working years, so it’s smart to find out what you may have coming to you and how to factor that into your budget during retirement.

How much will I get from Social Security when I retire?

The amount you’ll receive depends on a number of factors.

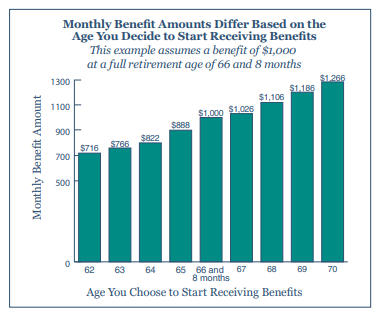

When you start taking Social Security will make a difference. The Social Security Administration says there’s no ideal age to begin receiving retirement benefits but, generally, the longer you wait, the more you’ll get.

- Taking your benefit early can mean as soon as age 62, but your monthly amount will be reduced because you’ll be receiving your benefit for a longer period.

- Starting your benefit at full retirement age means age 66 if you were born between 1943 and 1954; the age gradually increases to 67 for those born in 1960 or later. The monthly payment would be higher than if you’d taken your benefit earlier, but lower than waiting until age 70.

- Waiting until you’re 70 years old will give you even more of a bonus. The longer you delay—up to age 70—the higher your monthly payments will be.

As you’re considering your options, you’ll want to think about life expectancy. Given that today’s 65-year-old is likely to live another 20 years,1 that’s a lot of years to plan for in retirement. If you’re married, you may want to factor in when your spouse is planning to take benefits. Since there are many strategies to consider, you may want to talk with your financial professional. Whichever timeframe you choose, be sure to follow the guidelines on applying for benefits.

What you earned during your working years is another important factor. Your monthly benefit is based on your highest 35 years of earnings. If you haven’t worked at least 35 years, your monthly benefit will be lower, as the years you didn’t accumulate earnings will count as zeroes.

Whether you’ll be taxed on your Social Security benefit is another consideration. It depends on other income you’re receiving—including pensions, your pay (if you’re still working), dividends, and other taxable income. If you need to pay federal taxes, you can have them withheld from your Social Security benefits. Some states also tax Social Security benefits, so be sure to check with your state tax agency.

One more thing to think about—Social Security is projected to face a shortfall in 2035 when trust fund reserves may not be enough to cover all of the benefits due because the population is aging, changing the ratio of workers paying into the system versus retirees taking benefits out.3 It bears watching as we get closer to that time period.

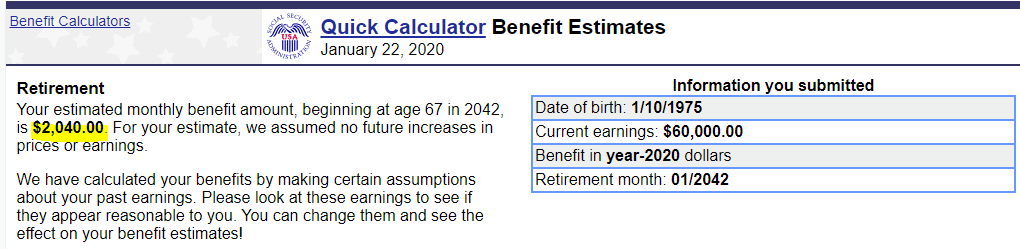

Calculate your Social Security benefit

Use our Quick Calculator to estimate your benefit. Being informed can help you avoid surprises when it’s time to apply. You can also get more information here, including setting up your account, determining whether you’re eligible for other Social Security benefits, and reviewing your statement.

Remember that Social Security is a great way to supplement your income in retirement. That’s why it’s important to save as much as you can through other sources, such as your 401(k) or other retirement plan benefit. It can help you be more financially prepared for the type of retirement you have in mind.

Important disclosures

Important disclosures

Source: “Your Retirement Checklist,” Social Security Administration, June 2019; “When to Start Receiving Retirement Benefits,” Social Security Administration, January 2020.

1 “Social Security Program Fact Sheet,” Social Security Administration, December 2019. 2 “Usual Weekly Earnings of Wage and Salary Workers Fourth Quarter 2019,” U.S. Department of Labor Bureau of Labor Statistics, January 2020, https://www.bls.gov/news.release/pdf/wkyeng.pdf. 3 “Fast Facts about Social Security," Social Security Administration, 2019.

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

MGR021020508544