Why financial stress is like the big bad wolf

For six years, John Hancock has surveyed retirement plan participants to learn how their personal finances affect their retirement savings, and we’ve seen financial stress increase, whether financial situations have gotten better or worse. With financial stress continuing to build, people have a hard time saving, which may leave their retirement plans as vulnerable as a house of straw.

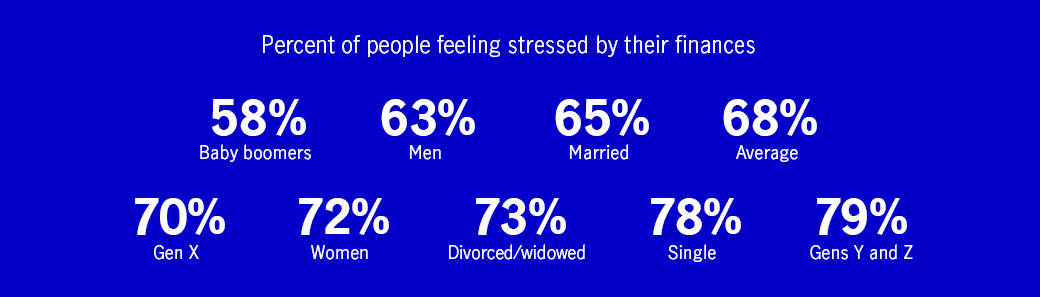

Financial stress hits more than two-thirds of workers

Sixty-eight percent of workers say that their finances cause them stress, and even though people feel better about their financial situation than they did six years ago, there are indications that this could be on a downward trend. Along with this year’s drop in the number of people rating their financial situation good to excellent, we see some troubling undercurrents. More participants are saying:

- Their financial situation is worse than two years ago

- They’re worried they may have financial difficulties

- They’re worried about losing their job

Financial stress isn’t evenly distributed, as some experience more than others. Generations Y and Z feel the most financial stress, followed by singles, divorced/widowed people, women, and Generation X. On the low end of the financial stress scale, baby boomers are the least stressed, followed by men and married/committed partners.

The causes of financial stress and how they delay retirement savings

The top two financial issues causing people stress are saving for retirement and saving for emergencies; the top two reasons people aren’t saving more for retirement are poor spending habits and debt.

Debt is one of the most significant indicators of financial stress, and most people are dealing with some kind of debt. Fifty-nine percent say their debt is a problem, with more than one in five saying it’s a major problem, and debt is a complicated factor that has ripple effects. Among people who say their debt is a major problem:

- 91% are financially stressed

- 79% are behind schedule in saving for retirement

- 62% have no emergency savings

But debt isn’t the only stressor, and the causes of stress vary. Baby boomers are concerned about the cost of healthcare, women are concerned that Social Security and Medicare won’t be available to them, lower-income households worry about a downturn in the economy, and millennials and Generation Z are worried about student loan debt.

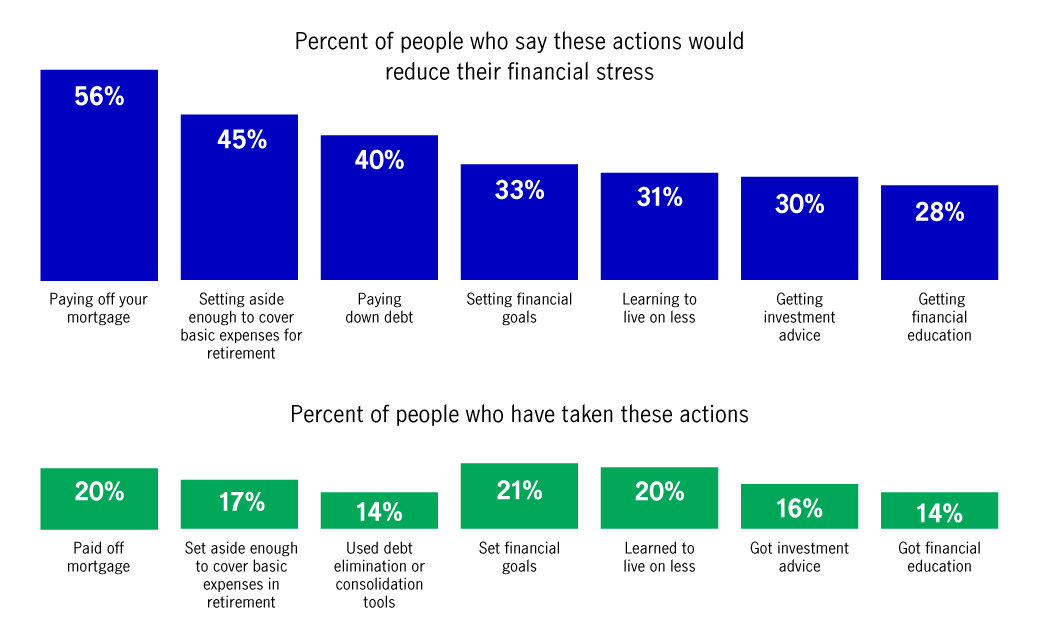

Financial wellness requires action, and action requires knowledge

Most people know what types of actions they should be taking to improve their situation and lower their stress. The problem is that the gap between what people know they should do and what they’re actually doing continues to grow.

Why aren’t people taking action? Debt and other financial obligations get in the way, and they don’t know how to take action. Few people consider themselves very knowledgeable about basic financial concepts.

- 33% say they’re very knowledgeable about managing debt

- 31% say they’re very knowledgeable about budgeting

- 20% say they’re very knowledgeable about personal savings

- 14% say they’re very knowledgeable about retirement savings

This shouldn’t come as a surprise, as only 17 states require financial education in high schools, leaving most people without easy access to personal financial education, but without knowledge, people either do nothing or do the wrong thing. What’s worse, having no shelter or building one out of straw and thinking it’ll be enough?

Financial illiteracy has a considerable impact on retirement, as a quarter of participants are willing to spend the time planning for retirement but don’t know how to start.

Financial wellness programs to the rescue

That’s where financial wellness programs come in. Employers have embraced financial wellness programs, understanding the importance of financial well-being for overall health. Almost two-thirds of employers say "financial well-being has gained more importance at their organization over the last two years. No employers say its importance has lessened.”

In order to help, financial wellness programs must educate people on the basics so that they know how to improve their situation. But the programs need to go a step further, with personally relevant solutions to motivate people to take action.

People expect a personalized approach. Participants say they’d save more if they had projections of their own expenses in retirement, as well as projections of their account balance in retirement, so they could look into what their lifestyle will actually be like in retirement. We have to teach people how to build toward financial wellness, as well as give them the tools they need for their own situation.

Some key takeaways

Financial stress is increasing, and everyone encounters it in different places along their journey to retirement. And while many people have an idea of what they should do to improve their finances, very few know how to actually take the necessary action. Financial wellness programs should address the core causes of financial stress—such as debt and competing financial obligations—with education and personalization. With a strong foundation, participants’ personal finances will have a better chance at withstanding whatever the big bad wolf blows their way.

Important disclosures

Important disclosures

John Hancock and Greenwald & Associates are not affiliated and are not responsible for the liabilities of the other.

John Hancock's sixth annual financial stress survey, John Hancock, Greenwald & Associates, 2019. A survey of more than 3,500 workers to learn more about individual stress levels, their causes and effects, and strategies for relief.

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. John Hancock does not provide investment, tax, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made here.

MGS-P40696-GE 11/19 40696 MGR110719503147