How to manage your 401(k) through market fluctuations

The COVID-19 outbreak has created uncertainty that’s shaken economies and stock markets around the world. If you’re concerned about what the ongoing fluctuations in the market mean for your 401(k) plan, you’re certainly not alone. Understanding how the stock market and your retirement plan strategy work together can help you make decisions amid all the uncertainty.

Stock markets and the value of investments have continued to swing up and down as investors try to guess how the COVID-19 pandemic will affect economic growth. Remember that your retirement plan is a long-term investment and market volatility is a short-term condition. These four short lessons can help you stay focused on your long-term goals.

Lesson 1: 401(k) investments have paid off in the long run

The stock market usually moves in anticipation of what the economy’s going to do, and markets fluctuate because investors are constantly changing their predictions about the future. These fluctuations are normal.

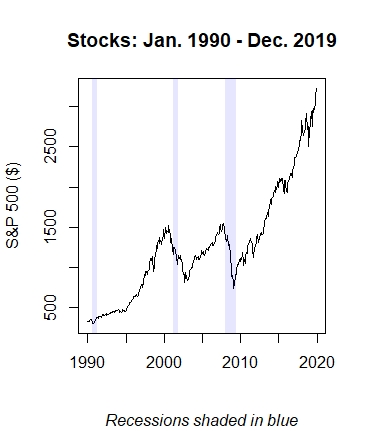

Taking a look at the growth of the U.S. stock market from January 1990 to March 2020 using the S&P 500 index, two long-term facts stand out:

1 Historically, stock prices have grown over the long term despite a lot of short-term choppiness along the way.

2 A recovery—and new highs—have always followed the occasional large setback.

In other words, the stock market has been resilient. Think about some of the large downturns that hit the U.S. economy between 1990 and 2020—caused by the terrorist attacks on September 11, 2001, the dot-com bubble bursting between 2000 and 2002, and the 2008/2009 financial crisis. In spite of all those downturns, people who started saving for retirement in 1990, 2000, and 2010 have all had access to significant stock market growth.

This makes investing in the stock market a powerful way to help build retirement wealth, but because recoveries tend to be sharp, fast, and unexpected, consider staying invested. Selling investments when the market turns south could increase the chance of missing out on the early stages of the eventual recovery.

Lesson 2: your 401(k) strategy should reflect how much time you have until retirement

While the stock market has been one of the best ways to build wealth over the long term, it’s also been one of the most volatile and unpredictable investments over the short term. That’s why you always need to consider how much time you have until retirement when building out your investment strategy. Younger investors who have time on their side and can afford to take more risk often make larger allocations to investments with higher potential returns. Investors who are approaching retirement and don’t have a lot of time to wait for a market rebound to offset possible losses tend to be more risk averse—and may not invest as heavily in stocks.

In other words, your retirement savings and investment strategy should reflect the fact that stock market investment risk goes down with time. If you have a long time until you plan to retire, you may be able to afford riskier investments; similarly, the closer you get to retirement, the less risky your investments should be.

Lesson 3: diversifying your 401(k) investments can reduce risk

So far, we’ve learned that the longer you’re invested in the stock market, the better equipped you are to build wealth—but you’ve probably also heard that you shouldn’t put all your investment eggs in one basket. That’s why your 401(k) investment menu has more than one type of fund to choose from. Some funds are invested in stocks, some are invested in bonds, and others are invested in a mix. The reason? When stock markets fall, more conservative investments (such as bonds) can act as a buffer, limiting your losses and potentially preserving more of your nest egg.

Let’s use two investors as an example and see how their hypothetical investment mixes make it through different market conditions. The first investor uses only a stock market fund and the second diversifies with 70% in stocks and 30% in bonds. We’ll see how they do in two falling stock market scenarios and two rising stock market scenarios.

Scenario |

Investor 1 (100% stocks) |

Investor 2 |

Stocks fall 25% and bonds go up 5% |

–25% |

–16.0% |

Stocks fall 10% and bonds stay the same |

–10% |

–7.0% |

Stocks go up 10% and bonds fall 1% |

10% |

6.7% |

| Stocks go up 20% and bonds fall 2% | 20% |

13.4% |

There is no guarantee that any investment strategy will achieve its objectives. Diversification does not guarantee a profit or eliminate the risk of a loss.

Although the diversified investor, Investor 2, didn’t gain as much when the stock market was up, Investor 2 also didn’t lose as much as Investor 1 when stocks were down. This simple example shows how investing in funds with different objectives can help reduce overall risk.

There are many different types of investments that you can use to diversify your 401(k), and some investments, such as asset allocation portfolios, provide one-step diversification by using one option. Or your 401(k) might offer you personalized advice based on your financial situation and goals. But the underlying principle to all these portfolio-building approaches is the same—using diversification to help reduce risk and smooth out returns.

Neither asset allocation nor diversification guarantees a profit or protects against a loss. An asset allocation investment option may not be appropriate for all participants, particularly those interested in directing their own investments.

Lesson 4: successful retirement planning depends on dollar cost averaging

Most people don’t think of falling stock markets as an opportunity, but they can be. In fact, occasional market setbacks have allowed investors who kept contributing to their 401(k) to buy shares at relatively low prices.

The saying goes, buy low, sell high. When you keep contributing to your 401(k) in a falling stock market, you’re buying low and getting more shares of an investment with each contribution dollar. Over time, buying low may help reduce your average cost per investment, which is known as dollar cost averaging.¹

Tying it all together

These lessons sound good in theory, but how do you stay the course when markets get really rocky?

Don’t react to short-term performance. Market swings aren’t a good representation of long-term trends. Consider staying invested to realize the full wealth-building potential of the stock market.

Review your strategy. If your investments were diversified and based on your goals and expected time to retirement before this bout of stock market volatility, then your best bet could be to change nothing. If your strategy still aligns with your goals, you should probably consider staying the course.

Keep your emotions in check. When you’re feeling anxious, remember that, over time, the stock market has recovered and grown.

Remembering these lessons will help ensure that the short-term volatility created by the coronavirus doesn’t do lasting harm to your plans for retirement.

Perspectives on market volatility

Visit our market volatility resource page for more helpful articles about the financial markets and the economy.

Important disclosures

Important disclosures

For complete information about a particular investment option, please read the fund prospectus. You should carefully consider the objectives, risks, charges, and expenses before investing. The prospectus contains this and other important information about the investment option and investment company. Please read the prospectus carefully before you invest or send money. Prospectuses may only be available in English.

It is your responsibility to select and monitor your investment options to meet your retirement objectives. You should review your investment strategy at least annually. You may also want to consult your own independent investment or tax advisor or legal counsel.

You should always keep in mind, though, that you cannot count on the market to behave the same way in the future as it has in the past. These comparisons, while a helpful way to evaluate your investment options, should not be considered predictors of future performance.

There is no guarantee that any investment strategy will achieve its objectives.

A widespread health crisis, such as a global pandemic, could cause substantial market volatility, exchange-trading suspensions and closures, affect the ability to complete redemptions, and affect fund performance; for example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other preexisting political, social, and economic risks. Any such impact could adversely affect the fund’s performance, resulting in losses to your investment.

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

MGS-P41949 GE 5/20 41949 MGR0519201183213