Five steps to help you meet your retirement savings goal

Most of us experience some level of financial stress, including 65% of couples and 78% of singles.¹ No matter where you are in your personal life, there are simple steps you can take to help relieve some of that pressure and get in a better position to meet your long-term goals.

Stepping closer to retirement readiness

Chances are good that you’ll spend a lot of years in retirement, given that a 65-year-old today is likely to live another 20 years.2 The good news is that there are ways you can help yourself and limit your financial stress, one step at a time.

STEP 1

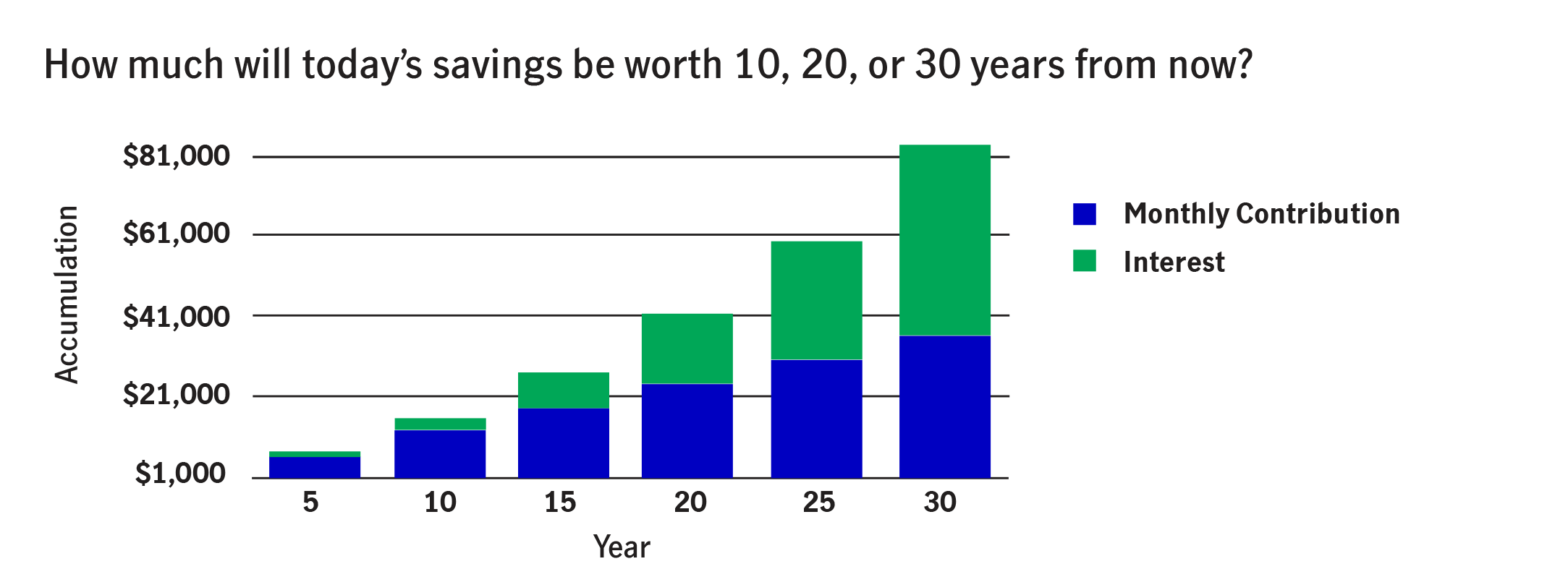

Start early and build your savings over time. Whether you’re saving through an IRA or an employer-sponsored plan, such as a 401(k), your retirement plan investments generate earnings. Those earnings are reinvested and generate their own earnings. That’s called compounding, and the earlier you start saving, the more powerful the effect of compounding.

Use a tool, such as the contribution calculator, to see how your contributions today can grow over time. Over 30 years, monthly contributions of $100, for example, would total $36,000. But if those contributions are invested and earn a 5% annual return, the compounded interest alone is $47,232, with a total balance of $83,232—more than twice the original contributions.

This hypothetical example does not reflect the deduction of taxes or transaction costs. There are risks associated with investing, including, but not limited to, loss of principal. There is no guarantee that any investment strategy will achieve its objectives.

STEP 2

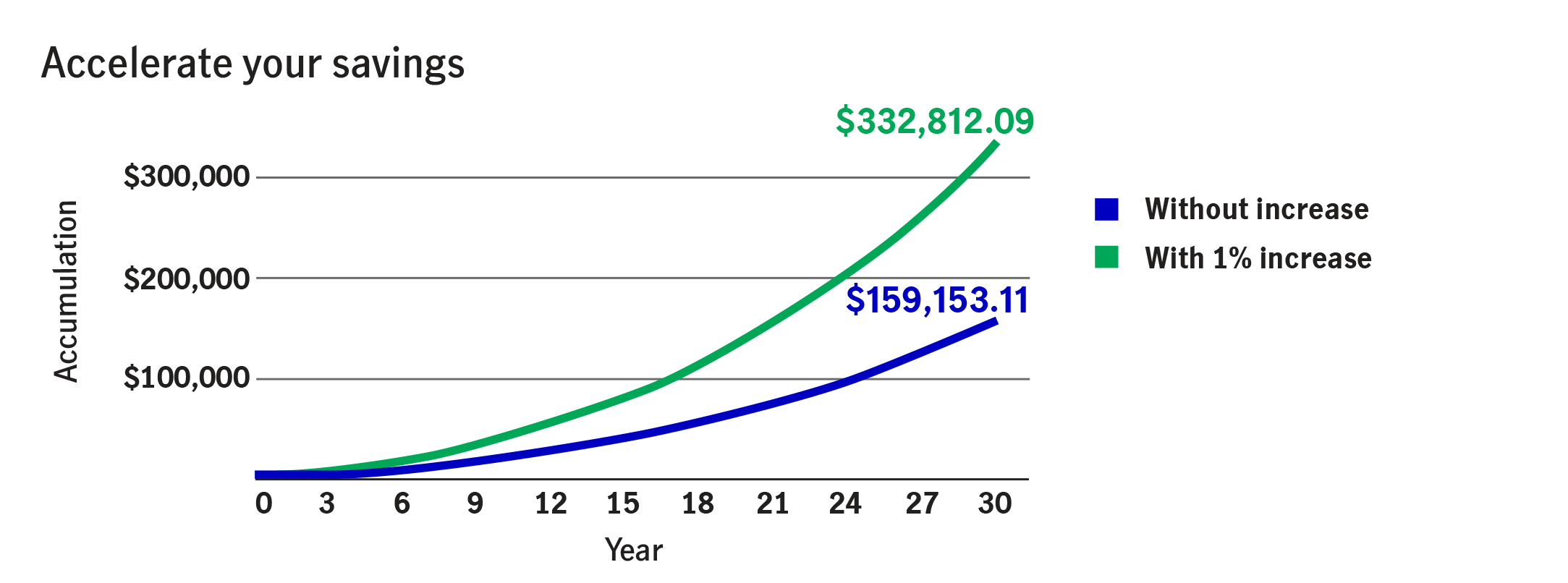

Increase your contributions as your income goes up—it can help make a big difference to your retirement savings over the long term.

Even raising your contribution percentage by as little as 1% per year can lead to significantly higher savings over time. What if you increased your contribution 1%—from 3% to 4%? Assuming a $40,000 annual salary and a 5% rate of return, you could more than double your savings over 30 years, from $159,153 to $332,812.

The maximum you can contribute to a 401(k) in 2020 is $19,500, so you can keep increasing until you reach the limit.

This hypothetical example is based on a mathematical principle and represents no particular investment. It does not reflect the deduction of taxes or transaction costs. There are risks associated with investing, including, but not limited to, loss of principal. There is no guarantee that any investment strategy will achieve its objectives.

STEP 3

Catch up, if you’re 50 or older, with catch-up contributions. It’s especially helpful if you’ve gotten a late start in saving—or feel that you’ve fallen behind. The 2020 catch-up contribution maximum is $6,500—allowing you to save a total of $26,000 per year in your 401(k).

STEP 4

Diversify your investments by spreading your savings among different asset classes (e.g., cash, bonds, and stocks). Diversifying may help you manage the overall market ups and downs and risks associated with your portfolio. When one asset class performs well, those gains can help offset other asset classes in your account that aren’t performing as strongly.

Neither asset allocation nor diversification guarantees a profit or protects against a loss. There's no guarantee that any investment strategy will achieve its objectives.

STEP 5

Track your progress regularly after you’ve put your plan together by reviewing your retirement savings balance and seeing how your investments are doing. When you monitor your progress, you can make adjustments as needed, either by saving more or changing some of your investments. As you’re calculating how much you’ll have in retirement, don’t forget to factor in your estimated Social Security benefit, which will be an important source of your retirement income.

Be careful not to derail your retirement savings

Out-of-control expenses can have a negative effect on even the most carefully planned retirement strategy. Planned expenses, such as mortgage or rent or financing and maintaining a car, should be part of an overall budget. Having a safety net for unplanned expenses, such as a major household repair or medical emergency, is also important. To help prepare for unforeseen events, building an emergency savings budget that covers three to six months of expenses can help make a difference. It can help you avoid using credit cards or borrowing money—or even taking a break in saving through your retirement plan, which could affect your long-term financial goals.

Achieve your retirement savings goal—you can do it!

Starting early and planning ahead can make it easier to meet your retirement savings goal. Estimate how much you’ll need in retirement and how much you need to save. Review your employer-sponsored retirement plan to be sure you’re contributing enough, then track your savings and investment progress periodically. It’s never too late to start—so if you’re not saving yet, start now!

Important disclosures

Important disclosures

1 John Hancock’s sixth annual financial stress survey, John Hancock, Greenwald & Associates, June 2019. A survey of more than 3,500 workers to learn more about individual stress levels, their causes and effects, and strategies for relief. 2 “Social Security Fact Sheet,” Social Security Administration, June 2019.

This content is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

MGR032020511098