Evidence-based ideas for a 401(k) plan design upgrade

A key reason for John Hancock’s state of the participant research is to find the plan design and engagement elements that make a difference in workers’ retirement readiness. If you’re looking for effective enhancements to bring to your participants or clients, we offer evidence in favor of an auto feature, default contribution rate, or investment education upgrade.

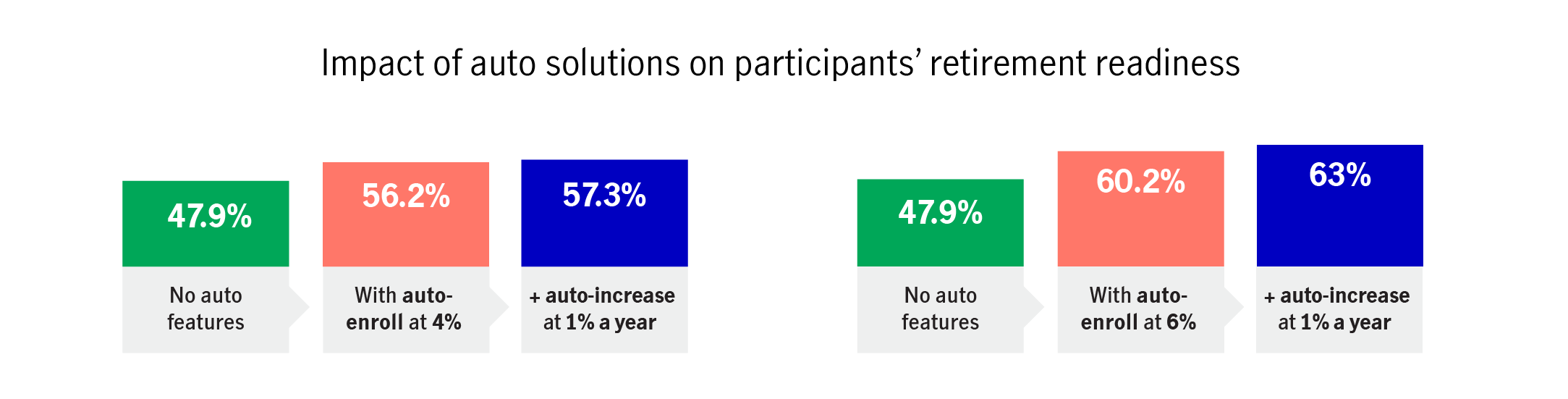

Auto-enrollment and other auto features are doing their jobs

The conventional wisdom is that automatic enrollment and automatic increase (which escalates employee contribution rates each year) will make a difference in supporting retirement readiness.1 Our participant data shows just how powerful those features are in combination.2

By adding auto-enrollment and auto increase, plan sponsors can expect planwide retirement readiness to increase significantly. We’ve seen 15% more participants achieve retirement readiness when plan sponsors use auto-enroll, a default contribution rate of 6%, and automatic increases of 1% per year.

Participants are accepting higher default contribution rates

Logically, you’d think that the higher the auto-enrollment default contribution rate, the more likely eligible employees would be to opt out; however, that’s simply not the case.

Our data indicates that a plan sponsor can push the default contribution rate up to—and even past—6% of salary without worrying about more participants opting out. Depending on the employer match formula, this could result in the total contribution percentage surpassing 10% of a participant’s earnings, and that’s a healthy starting point for building 401(k) savings.

Timely participant communications and education are helping to keep people on track

Late this past February, as the health crisis spread and the stock market started to react, we applied some of what we learned in the Great Recession of 2007/2008. We quickly took action to help educate 401(k) participants about the nature of market volatility and what it means for long-term savers.

In fact, we started delivering content in all channels we have—email, call center, and website—to help folks understand the difference between short- and long-term volatility and the importance of saving for the future. Just as important, we supported the efforts of plan sponsors by making a wealth of materials readily available online, for free.

While other factors have certainly played a role (including investors’ faith in their target-date funds and managed accounts, as well as simple inertia), timely and targeted learning has helped keep participants on track through a highly turbulent spring.

A review of our participant behavior from March through mid-May of 20203 showed that over 9 out of 10 participants:

- Stayed with or increased their deferral percentage

- Avoided taking a coronavirus-related distribution or other type of in-plan withdrawal

- Resisted borrowing from their 401(k)

- Stuck with their investment mix

As we’ve all learned—twice—over the last decade and a half, a sound educational and guidance strategy can help participants make thoughtful decisions when the markets turn challenging. Over time, this can be an invaluable benefit.

Tips for when you’re ready to enhance your plan

In times such as these—in fact, at any time—401(k) plan design will help shape the behavior that’s so important to a participant’s long-term success. You can encourage greater retirement readiness among your employees by considering:

- Adding auto-enroll, if yours is still among the 50% of plans that don’t use it4

- If using auto-enroll, raising the default contribution rate or linking in an auto-increase benefit

- Building a system for keeping participants educated and informed through ever-changing market conditions

With a few well-planned adjustments, your plan can be working harder and smarter for your participants and organization for years to come.

Full details on “State of the participant 2020,” including a download of the white paper, are available here.

Perspectives on market volatility

Discover our latest thinking and educational content to help participants get through market fluctuations.

Important disclosures

Important disclosures

1 John Hancock defines retirement readiness as the expected ability of a participant’s projected assets at normal Social Security age to replace at least 70% of their preretirement earnings. 2 Data is as of 9/30/19, from John Hancock’s open-architecture platform, which included 1.2 million participants, 1,123 plans, and $77.48 billion in assets under management. 3 Open-architecture platform data as of spring 2020. 4 “2019 Defined Contribution Recordkeeping Survey,” PLANSPONSOR, 2019.

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

MGTS-P41835-GE 06/20 41835 MGR0610201209855