Helping participants become better at 401(k) investing

Defined contribution plans tend to have three types of retirement savers: self-directed, who choose their own investments; moderately involved investors, who choose target-date funds; and managed account investors, who look for guidance on allocation and investment choices. To find out how the first two approaches are faring, our analytics team took a look at how John Hancock participants are managing their portfolios. It’s part of the research behind our "State of the participant 2020" study.¹

Most self-directed 401(k) investors might need a nudge

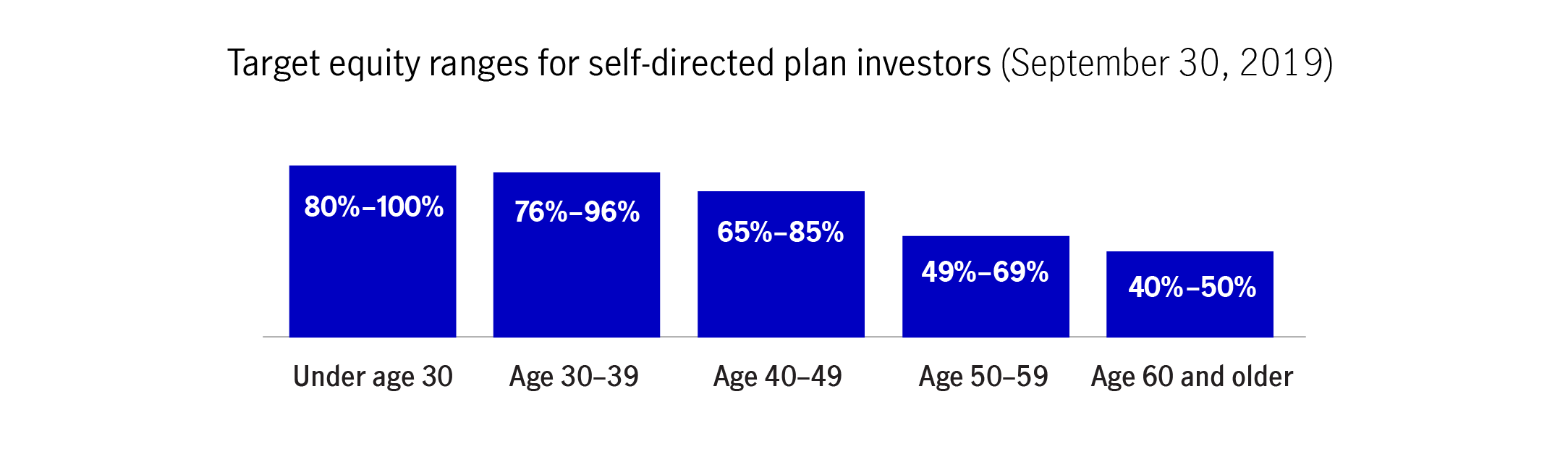

To see how well self-directed investors2 are doing with their asset allocation strategies, we compared their holdings with John Hancock’s age-specific target equity ranges.

These target ranges are based on the need for participants to balance growth potential with risk management as they move toward retirement. The equity target starts at 80% to 100% of the portfolio for someone under aged 30, gradually lowering to a recommendation of 40% to 50% of the portfolio by age 60.

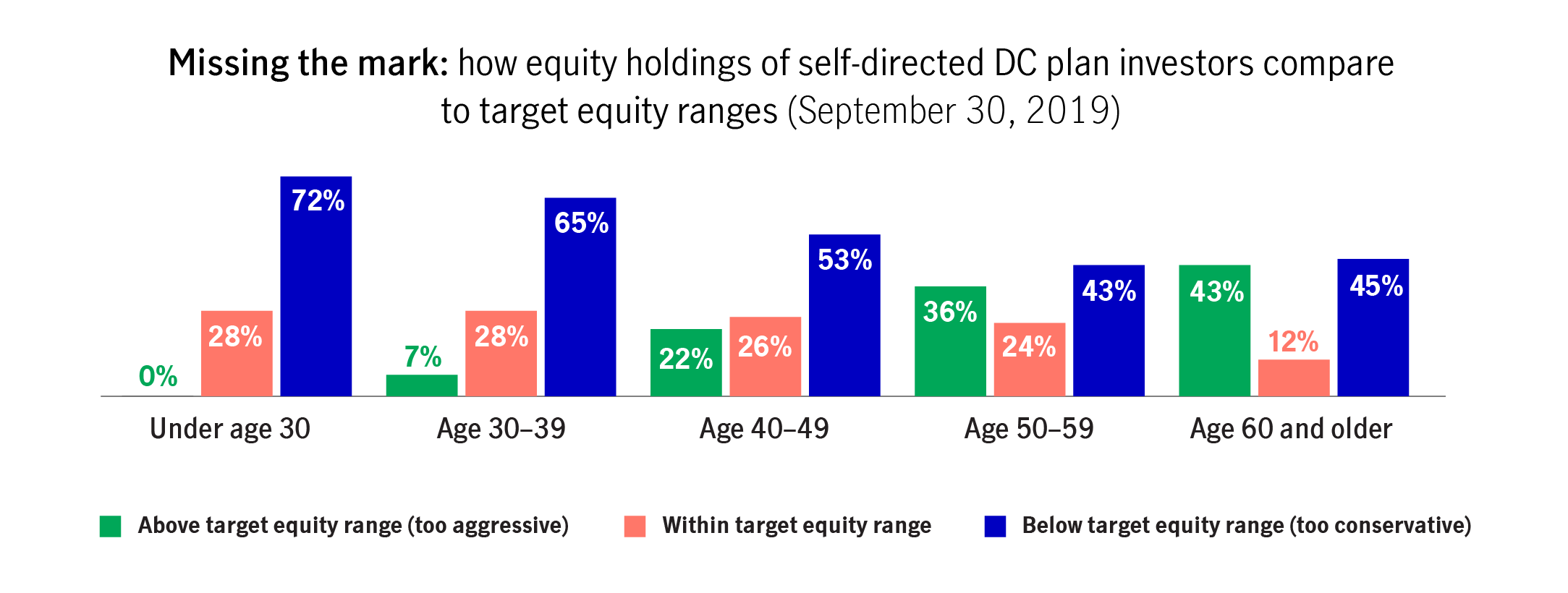

In comparing the holdings of self-directed investors against these targets, we discovered that relatively few hold an age-appropriate percentage of stocks. In fact, the percentage of self-directed investors who are on target ranges from only 12% to 28%, depending on what age group they’re in.

As you might expect, the likelihood of investing too aggressively grows as workers get older and the need for safety increases. But the bigger danger seems to lie in taking too little risk.

Overall, investors are perhaps too conservative, although that assessment gets slightly better with age. Almost three-quarters of retirement savers younger than 30 years old hold too little stock, with the remainder being appropriately allocated; none are overly aggressive.

The sliding scale changes with age, so that for people aged 60 and older, 45% are too conservative, 43% are too aggressive, and only 12% are appropriately allocated.

Education and plan design can help

To reach their retirement goals, self-directed investors need help understanding what makes up an appropriate investment mix—and what their options are if they don’t want to do it themselves. Retirement plan professionals can use this age-based data to develop targeted education and make plan design changes to help.

Education and engagement can help people understand the reasoning behind age-based asset allocation strategies. These are complex concepts for some, so the focus should be on using plain language to simplify them as much as possible.

For people who’d like a little more assistance, investment lineups should include target-date funds (TDFs) and target-risk funds, which can help to simplify the allocation issue. Managed accounts can be added for those who want someone else to do the investing for them.

Most TDF investors use them as intended

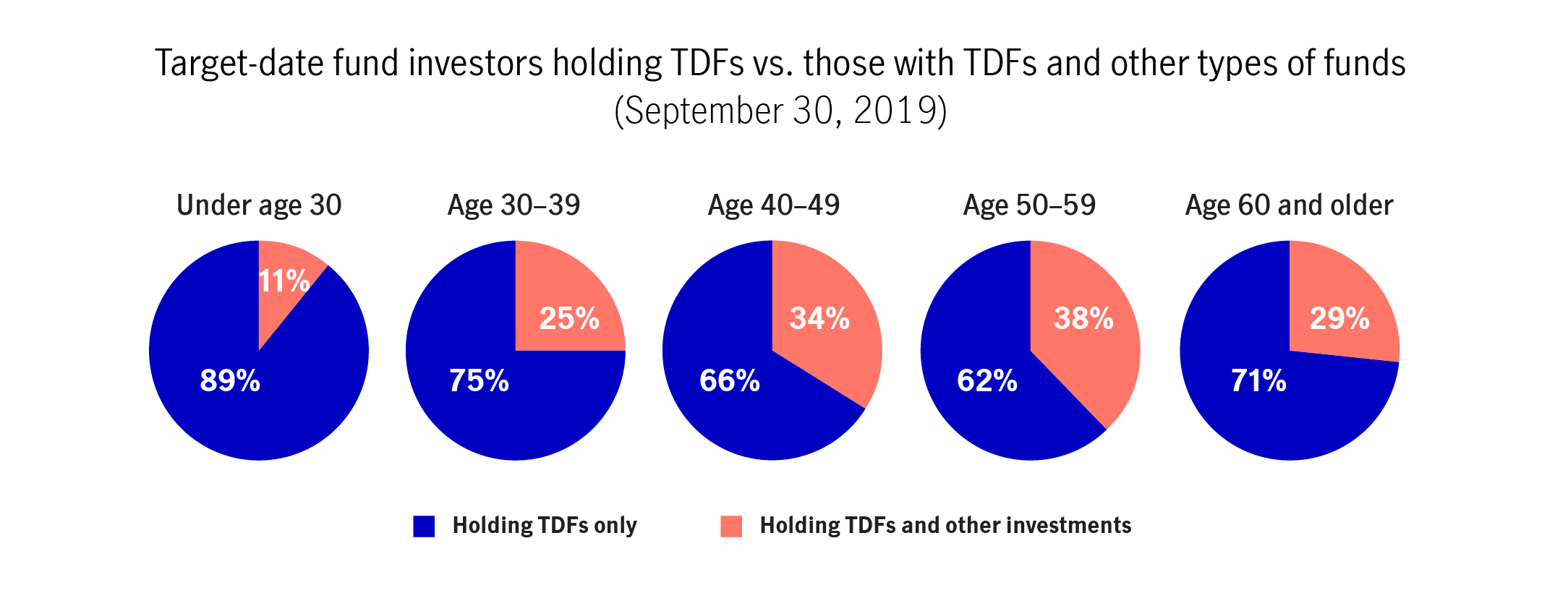

TDFs can help ensure age-appropriate investing when participants use them as intended. With a TDF, the manager continually adjusts the underlying mix of assets with a goal of maximizing returns earlier on and minimizing risk the closer the fund gets to its target date—the participant’s intended retirement date.

We looked at our participants to see how they’re using TDFs and found that the majority don’t hold any potentially conflicting investments. In other words, they’re using these funds as intended.

However, it seems that the longer they hold their TDFs, the more likely participants are to add other investments to their portfolio, potentially throwing the allocation off balance. Even as a TDF manager adjusts funds’ holdings and risks, an investor’s other investments can undermine the strategy by moving in their own direction.

Again, this is a scale that slides with age. While only 11% of participants under age 30 have mixed in other investments with their TDFs, 38% of those between ages 50 and 59 have done so. In some cases, participants may be intentionally adding these other investments to their TDF mix, but it’s likely that many are just unaware of the potential pitfalls.

Of course, participants investing in TDFs should monitor the asset allocation of the portfolio to make sure it’s consistent with their own risk tolerance. The principal value of the investment, as well as potential rate of return, isn’t guaranteed at any time, including at, or after, the target retirement date.

Education about 401(k) investing needs to align with plan design

When auto-enrollment is used to get people to participate, engagement and education can focus on how much to contribute. Likewise, TDFs—especially when used as a qualified default investment alternative—may be helpful in getting people into an age-appropriate allocation strategy. But it doesn’t end there.

Retirement plan professionals also need to provide guidance and education on the options for maintaining age-appropriate investments so that participants can build toward an anticipated retirement date and lifestyle.

For more on the current state of participants' habits and investments, see our complete "State of the participant 2020" study.

Important disclosures

Important disclosures

Neither asset allocation nor diversification guarantees a profit or protects against a loss. An asset allocation investment option may not be appropriate for all participants, particularly those interested in directing their own investments.

1 All data is from John Hancock’s open-architecture platform, which included 1.2 million participants, 1,123 plans, and $77.48 billion in assets under management, as of 9/30/19. 2 Self-directors exclude those holding one or two TDFs, in a managed or brokerage account, or invested in a custom model portfolio.

MGTS-P41600-GE 02/20 41600 MGR021920509560