How stable value funds work

Stable value funds are a type of principal preservation investment available to 401(k) plans, pensions, and other institutional funds. Understanding how a stable value fund works can help you determine if it’s right for your 401(k) or other institutional plan lineup.

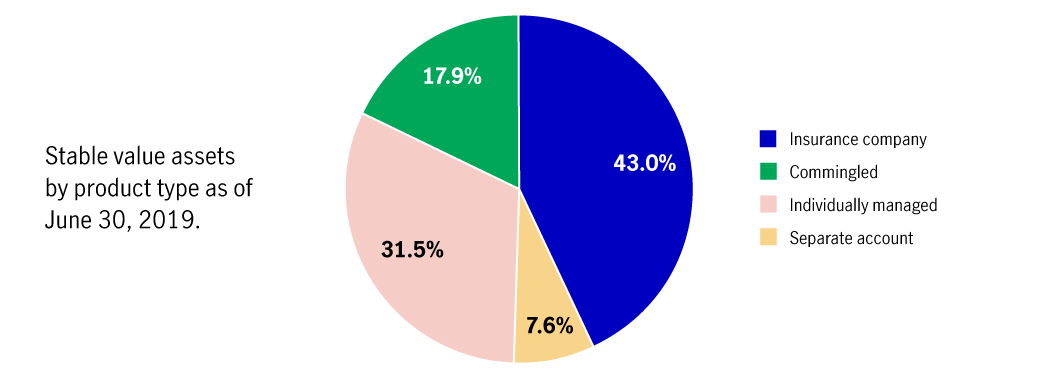

.png)

Why stable value?

Until the late 1970s, the options available for principal preservation were primarily money market funds and bank products. To give plans more choices and the potential to earn more income, insurance companies introduced stable value to pension funds. In the early 1980s, the 401(k) provided a new and growing source of demand for stable value funds. Today, stable value funds hold over $800 billion, or more than 10% of the $7.5 trillion U.S. retirement plan market.¹

Stable value's role in a 401(k) plan

401(k) plans have to offer a diversified investment lineup, which usually includes a principal preservation option. It’s up to plan fiduciaries to decide what type of fund to offer.

Stable value and money market funds both attempt to preserve capital while paying interest. It’s how stable value does this that makes it different. Though there are a few types of stable value funds, the two most prevalent are insurance company accounts and commingled funds.

Types of stable value funds

Insurance company account: An insurance company can create a stable value fund with assets in its general account. This type of stable value fund is an agreement between the insurance company and a plan sponsor, known as a group annuity contract. Under the agreement, the insurance company credits participant account balances with a guaranteed rate (the crediting rate); maintains a constant, daily, per-share price for transactions; and provides liquidity. A plan’s assets are invested in the insurance company’s general account, and the insurance company earns the difference between investment returns and the crediting rate. An insurance company account’s safety depends on the financial strength of the issuer.

If a plan’s assets are invested alongside the insurance company’s other general account assets, the account is referred to as a general account stable value product.

Commingled or pooled stable value fund: A commingled stable value fund is made up of a portfolio of bonds (which may be held in a commingled trust or in an insurance company’s separate account) and insurance company or bank-wrap contracts. Similar to an insurance company account, a commingled fund pays interest and allows for daily purchases and sales at a fixed price, a process accomplished through book-value accounting.

Like an insurance company account, a commingled stable value fund is only as safe as the financial strength of the insurance company or bank assurances that support it. But with commingled funds, many other companies can be guarantors.

|

Insurance company account |

Commingled fund |

Structure |

Group annuity contract |

Collective trust and/or pooled separate account subscription agreement |

Portfolio |

General account |

Bonds |

Plan exit |

Subject to restrictions |

Subject to restrictions |

Crediting rate |

Determined by issuer |

Determined by formula |

Minimum crediting rate? |

Usually |

Uncommon |

Guarantee backed by |

Financial strength and claims-paying ability of issuer |

Financial strength and claims-paying ability of the companies guaranteeing principal |

Source: “Stable Value Investment Association Quarterly Characteristics Survey for 2Q2019,” Stable Value Investment Association, 2019. Used with permission.

Stable value—the takeaways

Stable value funds can be used as a principal preservation option by 401(k)s and other institutional plans, providing participants both principal preservation and steady income. Prudent fiduciaries should understand stable value and the differences between insurance company accounts and commingled funds.

Important disclosures

Important disclosures

A fund’s investment objectives, risks, charges, and expenses should be considered carefully before investing. Refer to the Massachusetts contract for more details about the John Hancock Stable Value Guaranteed Income Fund.

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date but may be subject to change. It is not intended to provide investment, tax, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategy will achieve its objectives.

Stable value portfolios typically are invested in a diversified portfolio of bonds and entered into wrapper agreements with financial companies to prevent fluctuations in their share prices. Although a portfolio will seek to maintain a stable value, there is a risk that it will not be able to do so, and participants may lose their investment if both the fund's investment portfolio and the wrapper provider fail.

© 2019–2020 John Hancock. All rights reserved.

MGR-P41154-GE 1/20 41154 MGR011520505449