What to know before taking a loan from your 401(k)

Thinking of borrowing from your 401(k) to help pay expenses? You’re not alone. Many people explore this option when money feels tight. But tapping into your retirement savings now can affect the future you’re dreaming about, even when the loan’s repaid on time. So before you move forward, take a moment to understand how these loans work, their pros and cons, and possible alternatives that might fit your needs.

How 401(k) loans work

Here are the general rules that apply if your plan allows loans. We say if because not all plans offer this feature.

- Loan limits—The most you can borrow is generally the lesser of 50% of your vested account balance or $50,000. However, your plan may have a lower limit.

- Repayment period—You have to repay the loan within five years, unless it’s for the purchase of your primary home. And the payments must be made at least quarterly.

- Interest rate—You’ll have to pay interest on your loan, just like you would if you borrowed money from a bank. The difference is that the interest goes into your 401(k) account. Your plan sets the interest rate for your loan, and it’s typically tied to the prime rate.

- Fees—Your plan may charge you loan application and processing fees. These fees are taken from your account, not the amount you’re borrowing.

- Taxes—You’ll have to pay taxes on the loan if it isn’t repaid, and a 10% early withdrawal penalty if you’re under age 59½.

Pros and cons of 401(k) loans

Why would someone consider borrowing from their retirement account when they need money? There are a few reasons:

1 Preapproval isn’t required (although you may have to complete paperwork)

2 The interest rate is generally lower than what a bank may charge

3 You pay yourself back; the principal and interest go into your retirement account

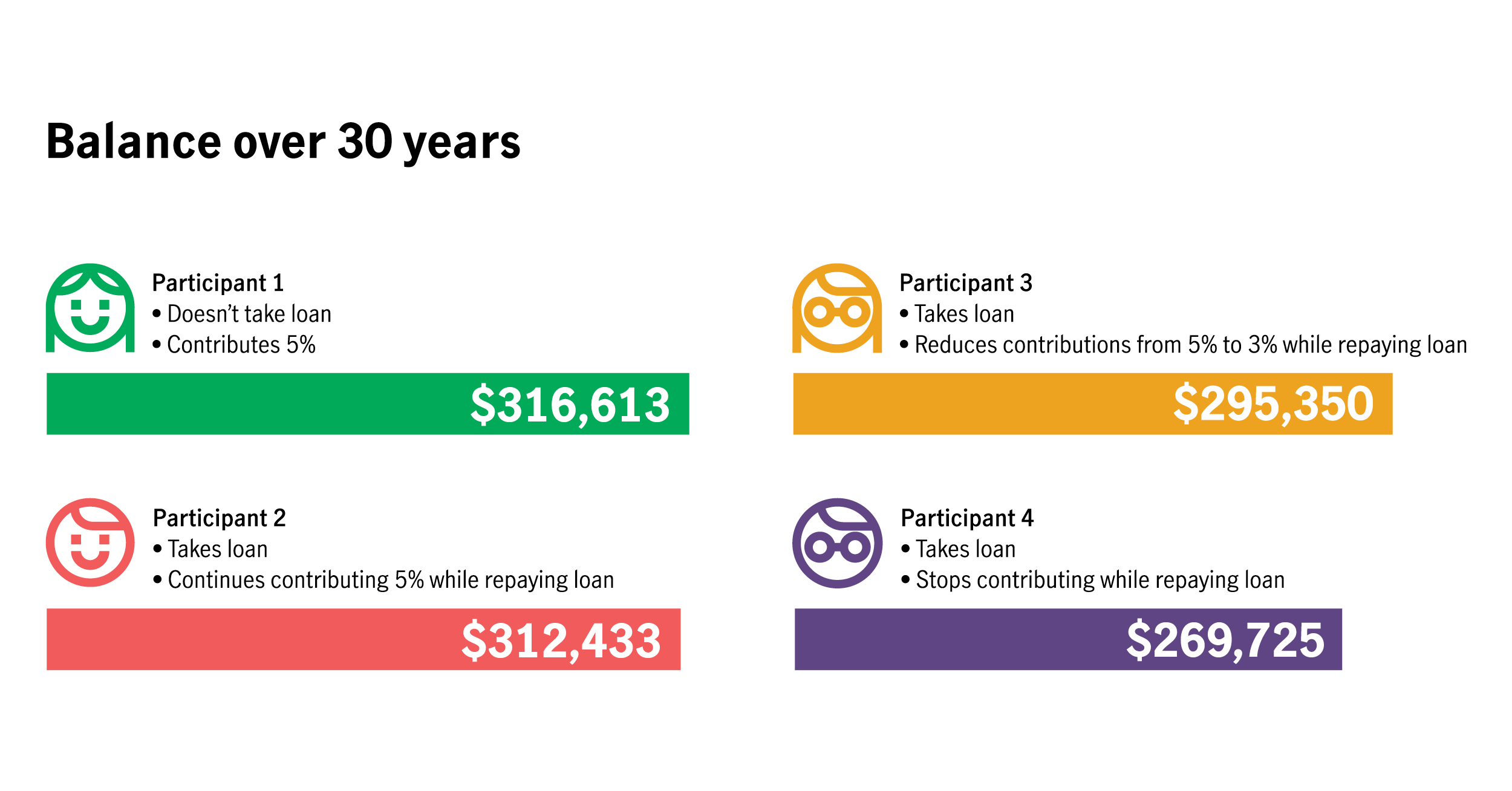

However, these benefits come with a significant downside, besides fees and possible taxes. When you take money out of your account, you miss out on the growth it might have earned. As a result, it may take you a lot longer to reach your savings goal. And it can be tough to catch up even if you keep contributing while you repay your loan.

Here’s an example of the potential impact a loan can have.

Alternatives to borrowing from your 401(k) account

For this reason, a 401(k) loan should generally be your last resort, after you’ve considered all your other options, such as:

- Cutting other expenses in your budget to help cover your immediate financial need

- Tapping into your emergency savings fund

- Withdrawing money from your non-retirement savings and investment accounts

- Borrowing from a bank or another financial institution

- Asking family members for support

Using one or more of these options may eliminate your need to take a 401(k) loan or reduce how much you have to borrow, helping you keep your retirement savings on track.

Borrowing responsibly

If, after thoughtful consideration, you decide a 401(k) loan is still your best option, consider these tips to help lessen the impact.

- Don’t take more than you need

- Keep contributing to your account

- Repay the loan in full as soon as you can

401(k) loans—a lifeline for emergencies, not everyday

A 401(k) loan can be a lifesaver when life throws you a curveball and your resources are limited. But it’s important not to treat your retirement account like a savings account. Remember, you’re setting aside this money for something bigger—your future.

FAQs

How much can you borrow from your 401(k)?

The IRS limit for 401(k) loans is generally the lesser of 50% of your vested account balance or $50,000. However, your plan can set stricter rules, including lower maximum loan amounts and limits on the number of outstanding loans. To help you understand the rules that apply to your plan, check your summary plan description.

What happens if you leave your job with a 401(k) loan?

When you leave your job, you have to repay the 401(k) loan within the time frame set by your plan. If you don’t, the outstanding amount will likely be deducted from your account balance as a loan offset. You’ll have to pay taxes on the amount you didn’t repay and a 10% penalty if you’re under age 59 ½. One way to potentially avoid these taxes is by rolling the offset amount into an eligible retirement plan by your tax filing deadline, including any extensions. Because the rules can vary by plan, you should check your summary plan description for details.

Is it a good idea to borrow from a 401(k)?

It’s generally not a good idea to borrow from your 401(k) plan unless you don’t have any other resources to cover an immediate financial need. That’s because when you take money out of your account, it reduces your retirement savings, and you miss out on the potential growth that money might have had. It can be tough to catch up even if you keep contributing while you repay the loan.

How long do you have to repay a 401(k) loan?

401(k) loans generally must be repaid within five years, with payments made at least quarterly. This time frame is set by the IRS. The one exception to this five-year rule is a loan to buy a primary residence. For this type of loan, your plan may allow a longer repayment period. Since repayment terms can vary, check your summary plan description to understand the terms that apply to you.

Important disclosures

Important disclosures

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice. Please consult your own independent advisor as to any investment, tax, or legal statements made.

MGR0327265327473