What does a target-date fund invest in?

If you have a workplace retirement plan, such as a 401(k), you’ve probably heard of target-date funds (TDFs). Often described as a one-step investment, a target-date fund is designed to keep investments aligned with a planned retirement date. But what’s actually inside one of these funds? Here’s a look at the three levels of investment management that help drive outcomes for TDFs.

What role could a target-date fund play in a retirement strategy?

When people are first introduced to a workplace retirement plan, one of their first questions is often, “How should I invest my money?” A target-date fund can supply a simple answer.

A TDF is designed to be a one-step investment, which means that it looks to provide a diversified portfolio of stocks, bonds, and other assets in a single fund. It seeks to balance growing savings long term while also protecting it against the risk of loss. What’s more, a target-date fund is meant to be held for an extended period—either to the date investors plan to retire or through their retirement years.

Individual TDFs are normally part of a collection of funds called a target-date fund suite. Within a suite, each fund has a year in its name (say, 2030 or 2055), and investors simply chooses the one that’s closest to the date they expect to retire.

Now let’s dig into the levels of investment management within each fund.

Level 1: the target-date glide path

The span of time between when someone begins saving for retirement to the date they expect to retire and no longer make contributions is called their investment time horizon. And the way an investor’s savings is optimally invested changes depending on where they stand along that horizon. The idea behind a target-date fund is to keep their investment strategy aligned with their horizon by automatically adjusting the relative balance of equities (or stocks), bonds, and other assets in the fund.

In the earlier years of saving, TDFs focus heavily on growing savings, which is where stocks play a key role. As an investor gets close to and actually enters retirement, the funds focus more on protecting savings by shifting from stocks to assets that have greater potential capital preservation properties, such as bonds and other income-generating assets.

The resulting pattern is called the fund’s glide path—which is the first level of investment management in a target-date fund. As you can see below, it’s similar to the maneuver pilots make in landing a plane. The green line is the expected percentage of stocks the TDF’s portfolio is expected to include1 along the investment time horizon.

A typical target-date fund glide path

.jpg)

Source: John Hancock Invetment Management, 2023. For illustrative purposes only.

Investors should examine the asset allocation of the portfolio to ensure it's consistent with their own risk tolerance. In developing the glide path, it's assumed that participants would make ongoing contributions during the years leading up to retirement and stop making those contributions when the target date is reached. The principal value of an investment, as well as the potential rate of return, isn't guaranteed at any time, including at, or after, the target retirement date.

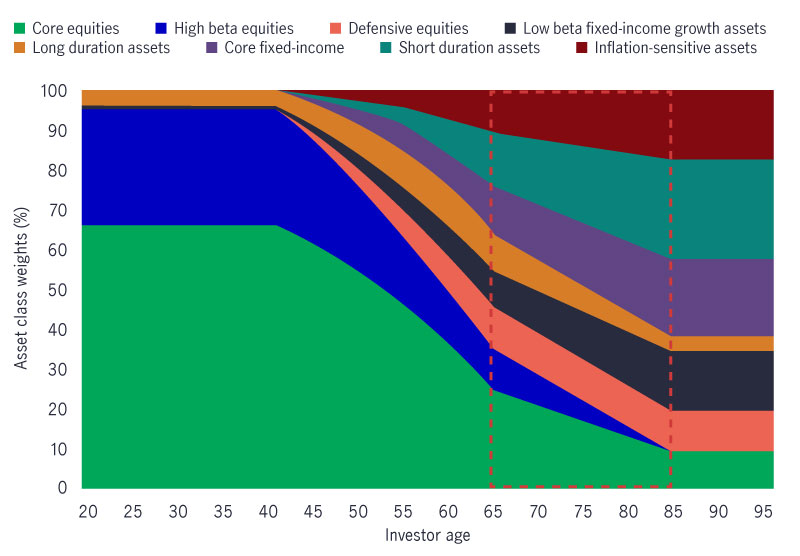

Level 2: asset class layering

The second level of investment management in a TDF involves picking broad categories of stocks, bonds, and other assets that will form part of the overall mix of assets in the glide path. This is called asset class layering.

Fund managers look for asset classes they think will work well together, and we define some of them a little later on. For instance, some asset classes (including core stocks and high beta stocks) are important because they tend to move in the same direction as the broader stock market. Other asset classes, such as long duration stocks and short-term bonds, may be chosen for their track record of capital preservation, even in down markets.

The following will give you an idea of how fund managers create layers of investments, each with a specific purpose, to compose a target-date fund. This asset class mix will shift over time as directed by the glide path—but also based on performance, economic and market conditions, and other factors.

Hypothetical asset class layering for a family of target-date funds

Asset class weightings by investor age

Source: John Hancock Investment Management, 2023. For illustrative purposes only. The area within the dotted lines represents the effort to decrease risk in the postretirement years.

Diversification and asset allocation do not guarantee a profit or eliminate the risk of a loss. There is no guarantee that any investment strategy will achieve its objectives. Investing involves risks, and past performance does not guarantee future results.

Although some of the asset classes above may not sound familiar to you, here’s what they may include:

- Core equities—Often refer to U.S. stocks and international stocks from other developed countries

- High beta equities—Such as small- and mid-cap stocks and emerging-market stocks, which can be riskier than the stock market as a whole (beta is a measure of relative volatility) but could also offer higher potential returns

- Defensive equities—Stocks that are generally less affected by the broader swings of the stock market and often provide lower returns but greater downside protection

- Low beta fixed-income growth—Typically include high-yield bonds, emerging-market debt, and bank loans

- Long duration assets—Assets with a longer time to maturity than 10 years

- Core fixed income—Often a mix of bond securities such as exposure to a broad bond index

- Short duration assets—Assets that typically mature in less than five years

- Inflation-sensitive assets—Assets that are used for inflation protection, such as real estate investment trusts (REITs) and Treasury Inflation-Protected Securities (TIPS)

- Alternatives—Typically include assets outside traditional fixed income and equity

Level 3: the fund’s underlying investments

Are you the kind of person who considers every ingredient in a recipe? Then you may want to look at the final level of investment management—the individual funds your target-date fund owns.

In this third level of investment management, a fund manager selects mutual funds, exchange-traded funds (ETFs), or other kinds of pooled investments to fill out an asset class strategy. While the number of underlying funds can vary, they’re chosen based on their style, composition, and the TDF manager’s performance standards and timeframes.

A given family of target-date funds might be built from these types of underlying investments:

Equity (stock) funds |

Fixed income (bond) funds |

Large cap |

Core |

Large-cap sector |

High yield |

Mid cap |

Emerging markets |

Small cap |

Short-term inflation protection (e.g., TIPS) |

International large/mid cap |

Long duration U.S. Treasury (e.g., STRIPS) |

Defensive equity |

Stable value funds |

Emerging markets |

|

Real estate investment trust (REIT) |

Source: John Hancock Investment Management, 2023. For illustrative purposes only.

TDF managers also typically consider things such as costs and fees when deciding on underlying investments. This, in turn, helps them determine whether a target-date fund should be mostly made up of mutual funds, ETFs, or a combination. Managers will also consider the most effective way to access a specific asset class.

For example, there are many equity ETFs that provide lower cost exposure to the broader stock markets and typically work well as part of a target-date fund. But it’s also important for a fund to take a more active approach to fixed income, which may make an actively managed ETF or mutual fund a better way to invest in bonds. TDF managers weigh all these considerations carefully when choosing underlying investments as part of a fund.

Participants can quickly discover what their plan’s offerings are invested in by going to their retirement plan website and looking at the fact sheets for the TDFs available to them.

Target-date fund managers use three layers of investing to help keep it simple

If someone is just getting started with retirement investing—or prefers a portfolio that’s managed for them—a TDF can be a good choice. By choosing the target-date fund that’s in line with their potential retirement year, an investor gets multiple levels of investment help, from the design of a glide path to the selection of underlying funds.

To help meet retirement goals, it’s critical to understand how the investment options in a retirement plan work. Consideration should also be given to contributing as much as possible as early as possible and to reviewing any investment strategy at least once a year.

1 In more technical terms, this pattern of decreasing equity holdings is called the target-date fund’s strategic weighting.

For complete information about a particular investment option, please read the fund prospectus. You should carefully consider the objectives, risks, charges and expenses before investing. The prospectus contains this and other important information about the investment option and investment company. Please read the prospectus carefully before you invest or send money. Prospectuses may only be available in English.

Important disclosures

Important disclosures

It is your responsibility to select and monitor your investment options to meet your retirement objectives. You may also want to consult your own independent investment or tax advisor or legal counsel.

A target-date portfolio is an investment option comprising a fund of funds that allocates its investments among multiple asset classes that can include U.S. and foreign equity and fixed-income securities. The target date is the approximate date an investor plans to start withdrawing money. The portfolio’s ability to achieve its investment objective will depend largely on the ability of the subadvisor to select the appropriate mix of underlying funds and on the underlying funds’ ability to meet their investment objectives. The portfolio managers control security selection and asset allocation. There can be no assurance that either a fund or the underlying funds will achieve their investment objectives. Investors should examine the asset allocation of the fund to ensure it is consistent with their own risk tolerance. A fund is subject to the same risks as the underlying funds in which it invests. Because target-date funds are managed to specific retirement dates, investors may be taking on greater risk if the actual year of retirement differs dramatically from the original estimated date. Target-date funds generally shift to a more conservative investment mix over time. While this may help manage risk, it does not guarantee earnings growth. An investment in a target-date fund is not guaranteed, and you may experience losses, including principal value, at, or after, the target date. There is no guarantee that the fund will provide adequate income at and through retirement. Consider the investment objectives, risks, charges, and expenses of the fund carefully before investing. For a more complete description of these and other risks, please see the fund’s prospectus.

This content is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made.

John Hancock Investment Management Distributors LLC is the principal underwriter and wholesale distribution broker dealer for the John Hancock mutual funds, member FINRA, SIPC.

John Hancock Retirement Plan Services LLC offers administrative or recordkeeping services to sponsors and administrators of retirement plans. John Hancock Trust Company LLC provides trust and custodial services to such plans. Group annuity contracts and recordkeeping agreements are issued by John Hancock Life Insurance Company (U.S.A.), Boston, MA (not licensed in NY) and John Hancock Life Insurance Company of New York, Valhalla, NY. Product features and availability may differ by state. Securities offered through John Hancock Distributors LLC, member FINRA, SIPC.

MGR0621232940306