Eight retirement plan goals for 2020

The beginning of the year is a good time to assess and adjust, and for retirement plan sponsors, it’s a good time to review last year’s plan data and goals and decide whether those goals are still right for their organization.

What are your priorities as a plan sponsor?

Making a retirement plan more effective over time involves the same approach as meeting other key business objectives. It requires establishing priorities and creating a plan to meet them. Here are eight goals that plan sponsors can aim for this year.

1 Improve financial wellness¹

Nearly 70% of defined contribution (DC) plan participants say that personal finances are a significant cause of stress. What’s the main cause of personal financial strain? Debt, specifically, student and credit card debt. Employers increasingly realize this, and the majority are planning on doing something about it—but many haven’t taken the first step. Plan sponsors should consider making 2020 the year that they improve worker financial wellness by:

- understanding the bottom-line cost of financial stress,

- measuring employee financial stress and overall wellness, and

- giving employees the tools to manage financial stress, enable whole-picture planning, and improve.

These tools should include help with budgeting, debt management, emergency savings, college planning, and student loans.

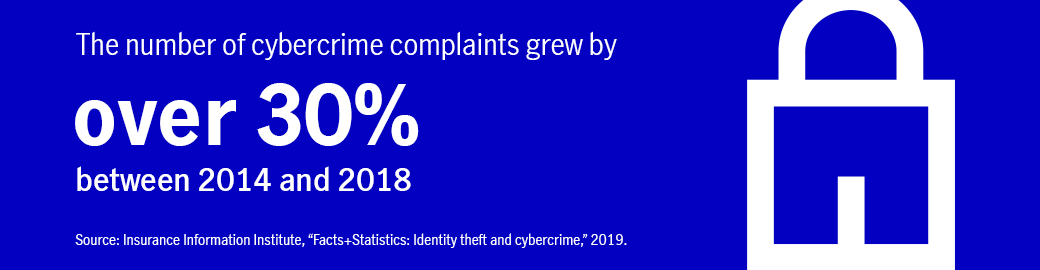

2 Strengthen cybersecurity

Employers have a duty to keep employee information and assets safe from cyber threats, and they can help to keep employee data secure by making cybersecurity a priority in the new year. This starts by partnering with a plan provider that helps protect employee accounts through:

- two-step verification,

- real-time transactions alerts,

- cooling-off periods for withdrawals following new online account access registrations,

- proactive account transaction monitoring to identify unusual or suspicious activity, and

- account holds when unusual or suspicious activity is detected.

Anyone can be a victim of a cybercrime, and cybercriminals are relentless.

Vigilance against threats to cybersecurity can help keep your employees’ information and retirement accounts secure in 2020.

3 Offer advice¹

When it comes to managing retirement assets, few employees have the time or training to act as their own investment advisor—67% of 401(k) plan participants say they want personalized, professional advice; only 12% have a written financial plan for retirement.

Managed accounts, available through DC plan providers and third-party investment advisors, can help. They’re accessible in a variety of ways: electronically, face to face, and over the phone. Managed accounts help improve participant financial wellness—participants who use them and who aren’t saving enough end up contributing more, and users realize improved account balance diversification.²

4 Design for your demographics

Plan design is an ongoing process. This is due partly to normal workforce turnover, but also to the evolving needs of employees as they age, and a plan has to adapt to keep in line with other competitors' benefits. Auto features, such as auto-enrollment and auto-increase, can help get your younger employees saving early. They should include:

- periodic auto sweeps of noncontributors (or low contributors) into the plan, and

- auto-enrollment into catch-up contributions.

Retiree needs are different. They typically want safety and income, and they may require:

- retirement income planning help;

- flexible withdrawals, including partial distributions and installments; and

- a high-quality principal preservation option and suitable income-oriented investments.

A plan’s design should reflect its sponsors goals and the unique needs of its workforce—needs that change from year to year. If a plan’s workforce and its needs are expected to change in 2020, plan design should adapt.

5 Review principal preservation choices

Both long- and short-term interest rates declined in 2019, pressuring money market returns and bond income. This makes generating retirement income while keeping principal safe more challenging in 2020.

Stable value is a principal preservation investment designed mainly for retirement plans. Historically, it's provided higher income than money market funds and other safety-oriented investments.³ For plan sponsors concerned with the impact of falling interest rates on retiree income, 2020 may be the time to consider offering a potentially higher-yield alternative to cash or money market funds.

6 Evaluate fees

Sponsors of ERISA-covered retirement plans have a duty to ensure that costs are reasonable relative to services provided. Although ERISA doesn’t require any particular schedule for evaluating costs relative to services, this duty is ongoing. Most plan sponsors regularly review costs relative to benefits and services. Plan sponsors should consider fees, service provider costs, and service reviews part of their agenda in 2020.

7 Use a compliance calendar

DC plan sponsors have to perform a number of tasks to stay in good standing with the IRS and the U.S. Department of Labor (DOL), and many of these tasks have deadlines. To keep up, plan sponsors can use a compliance calendar, which has information on important due dates for contributions, tax filings, corrective measures, and participant information. Examples of key deadlines are:

- January 15—Census data due

- February 15—Compliance testing results due

- March 31—Form 5500 completion due

- April 15—Employer contribution funding deadline

- July 31—Form 5500 filing deadline

- September 30—Summary annual report distribution deadline

Other required tasks, such as distributing annual notices to employees, can happen at any time during the calendar year. To help avoid late penalties—or, in extreme cases, plan disqualification—plan sponsors should consider keeping a compliance calendar on hand throughout the year and follow it closely.

8 Go digital

The American workforce is increasingly digitally dependent. Over two-thirds of employees consider their smartphone to be their main source of information and learning.⁴ By 2025, millennials—raised entirely in a digitally connected world—will make up 75% of America’s workforce.⁴ To fully engage with millennials and younger workers generally, retirement plans should commit to going paperless in 2020. This means offering digital:

- 401(k) enrollment,

- balance and benefit updates,

- 401(k) education and communications, and

- general communications and notification delivery.

This doesn’t just save paper—online enrollment leads to higher 401(k) savings rates and improved investment diversification.⁴ When combined with easy-to-access digital education and account maintenance tools, employees are more likely to stay engaged, but they can’t be completely engaged if a service provider doesn’t have their email address, so employers should make sure that their plan provider has up-to-date electronic records. This is particularly important if a plan sponsor wants to take advantage of the DOL’s proposed rule for electronic delivery of required plan disclosures.⁵ Although that rule won’t go into effect until 2021 at the earliest, plan sponsors can go a long way toward realizing the benefits of going digital by making sure that their service provider has current electronic records in 2020.

Remember to review and reset your goals

Retirement plans can’t stand still. They need to keep up with many different types of changes—legal, regulatory, economic, and social—and they need to adapt to an employer’s changing workforce and business goals. The beginning of a new year is a good time for plan sponsors to review their goals, but anytime there's a change, goals should be revisited and reset as needed. These eight areas are a good place to start.

1 Unless otherwise noted, all statistics cited are from John Hancock’s sixth annual financial stress survey, John Hancock, Greenwald & Associates, June 2019. A survey of more than 3,500 workers to learn more about individual stress levels, their causes and effects, and strategies for relief. 2 “The Impact of Managed Accounts on Participant Savings and Investment Decisions,” Morningstar, Inc., January 2019. 3 “Stable Value FAQ,” Stable Value Investment Association, 2013. 4 “A better path to 401(k) engagement: Three trends challenging the traditional approach,” John Hancock white paper, 2019. 5 "Fact Sheet: Retirement Plans Electronic Disclosure Safe Harbor Rule," U.S. Department of Labor.

Important disclosures

Important disclosures

Investing involves risks, including the potential loss of principal. There is no guarantee that any investment strategy will achieve its objectives.

Stable value portfolios are typically invested in a diversified portfolio of bonds and enter into wrapper agreements with financial companies to prevent fluctuations in their share prices. Although a portfolio will seek to maintain a stable value, there is a risk that it will not be able to do so, and participants may lose their investment if both the fund's investment portfolio and the wrapper provider fail.

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made here.

© 2019–2020 John Hanock. All rights reserved.

MGTS-p41447-GE 1/20 41447 MGR020320507868