Four questions to help align your retirement plan strategy with a planned M&A activity

Any retirement plan change calls for a skilled and coordinated effort, but when that change results from a merger, acquisition, or divestiture, diligent planning is especially important. Plan sponsors and their business partners should consider creating a comprehensive strategy as early as possible—preferably before the corporate action closes—so that all retirement plan transition options will be available. Answering some key questions can help you get these crucial projects off to a strong start.

In a recent survey, 401(k) plan sponsors listed specialized project support—specifically, the harmonization of retirement benefits as part of a corporate event—as one of the most valuable services a financial professional can provide.1

Because we consult with many plan sponsors with ongoing merger and acquisition (M&A) activity, we understand the necessary information that must be gathered and the critical action steps that must be followed. To get your strategy off on the right foot, start by answering these four questions:

1 What are we trying to accomplish with the retirement program transition?

Phrases such as lower costs, better efficiency, and more uniform benefits may jump to mind when you’re planning a change in your retirement program, especially when part of a merger or acquisition.

Dig a little deeper to uncover other strategic drivers behind the retirement program. Employee morale and commitment are common goals. Moving new employees effortlessly into their new 401(k)—with benefits at least as good as they’ve been used to—can help build goodwill.

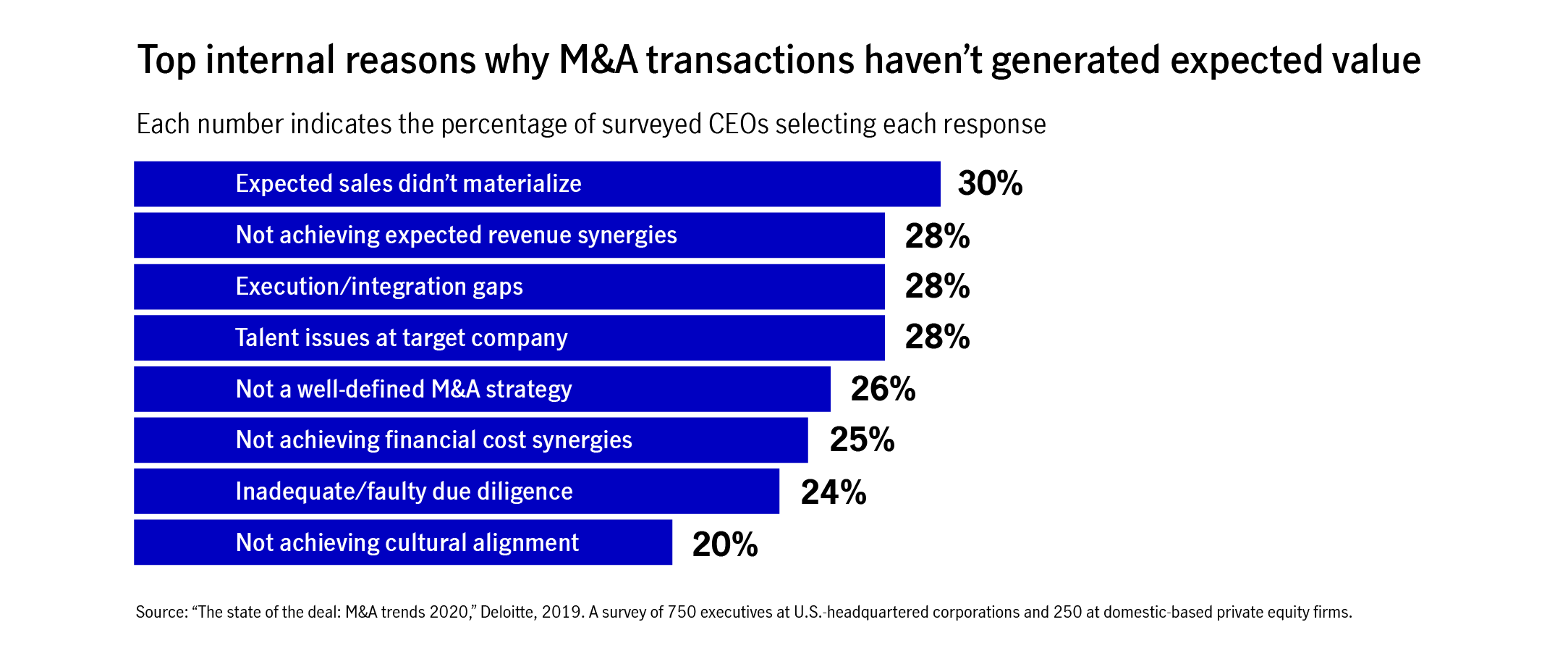

Why else might the transition be important? A group of 1,000 executives with M&A experience was recently asked why certain deals they were involved in didn’t deliver the outcomes they were seeking. Execution and integration, failure to achieve cost synergies, and inadequate due diligence were all cited by at least 24% of respondents.

All these factors can be addressed, in part, with a well-crafted retirement program transition strategy.

2 Do plan participants have a clear pathway to retirement?

Depending on the nature of the corporate action and design of the current retirement programs, there may be limitations on how the transition can work. If it’s an asset sale, affected employees may need to take responsibility for rolling their old 401(k) balances into their new plan. Nonqualified plan participants may be forced to take early payouts (and face unexpected tax liabilities) triggered by “change of control” provisions.

Make sure your strategy exposes and corrects these kinds of issues—with an eye toward encouraging retirement readiness for every individual.

3 Is the path clear for the business as well?

Even transitions that may sound straightforward—such as a 401(k) plan consolidation—can present plenty of potential challenges.

Take the time to work out the details.

- Does the seller’s plan have a history of failing nondiscrimination tests or other fiduciary risks? These risks could create liabilities for the buyer down the road.

- If defined benefit plans are in play, be aware that taking on new participants can cause a shift in the liability profile of the buyer’s plan. This could lead to the need for an adjusted asset allocation strategy.

- Think through the plan and participant impact regarding all potential updates to the design, benefits, and distribution options of the buyer’s 401(k) plan.

- Consider whether the changes might cause problems with the Employee Retirement Income Security Act of 1974 (ERISA) or the Internal Revenue Code, as well as how they’ll be communicated to participants.

4 Is your team of retirement plan experts on board and ready to tackle the project?

Of the 26 separate tasks we’ve identified as part of the retirement program transition process, 21 may be easier with appropriate help from a benefits consultant, consulting actuary, communications consultant, or the plan recordkeepers.

But advantages don’t end there. By assisting with due diligence efforts and plan design strategy, your team of experts helps avoid unpleasant surprises as the project unfolds.

When’s the right time to get your team started? Do it early in the process to create time for deeper analysis and better-informed decision-making—and to take advantage of plan transition options that may disappear once the corporate action date has come and gone.

For more details on how to plan a retirement program transition in support of a corporate action, download our guide for plan professionals.

1 “U.S. Retirement Markets 2019: Looking Toward Holistic Solutions for Participants and Plan Sponsors,” Cerulli Associates, December 2019.

Important disclosures

Important disclosures

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

MGTS-P41820-GE 3/20 41820 MGR031720510859