Six reasons to prioritize digital 401(k) learning

If you could design the ultimate learning system for your 401(k) plan participants, where would you start? Historically, onsite meetings were considered the gold standard, but enrollment methods, communication channels, plan designs, and employee expectations have changed. Here are six reasons why online learning may need to play a bigger role in your participant experience.

The new 401(k) plan basics include more and more online capabilities

1 Flexibility for 401(k) learning anytime, anywhere

Meetings on the web provide one advantage that onsite sessions simply can’t deliver: They allow people to learn wherever it suits them best. For some, a commuter rail ride may be the perfect time to pick up new financial skills; for others, it might be at the desk in the spare bedroom, the kitchen table, or wherever they tend to take care of personal financial business.

2 Virtual meeting tools can deliver an engaging, multimedia, and personal experience

Digital communication technologies can deliver much of the emotional impact felt from a live, face-to-face interaction. For larger meetings, webinar presentation platforms allow people to view the presenter—visual cues and all—and a compelling mix of graphics, videos, opinion polling, and real-time demonstrations of the tools they’ll be using. For smaller-scale meetings, video conferencing encourages ongoing, real-time discussions. These are the intangibles that spark engagement and lead to confident action.

3 The optimal 401(k) experience is all about smart automation

In the early days of the 401(k) plan, paper and pen ruled. Employees filled out enrollment applications with the help of very large, printed enrollment kits. In that kind of environment, face-to-face education and enrollment assistance made a lot of sense. Today, not so much.

Nearly half of plan sponsors use auto-enrollment to help get newly eligible employees off to a timely start, but even if your plan requires employees to initiate enrollment, automation can help.

A study of John Hancock’s recordkeeping data showed that all participants—including those earlier in their career (up to age 35) and in mid-to-late career (age 46 and older)—start off with higher deferral rates when they enroll online. Highest of all are those, across all age ranges, using our streamlined Express Enroll option.1

.png)

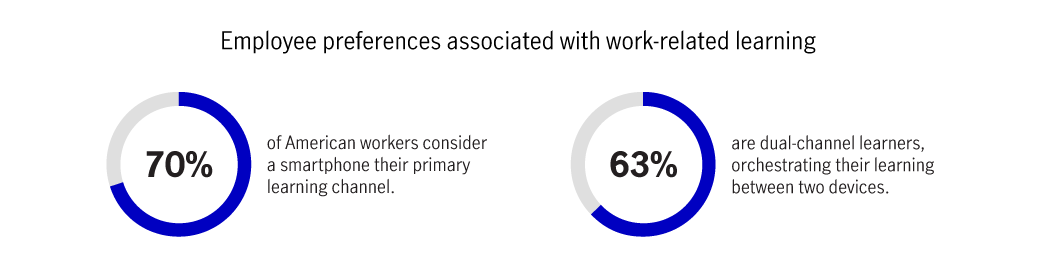

4 Workers prefer online learning

If given a choice between sitting in a conference room or in a spot of their choosing, guess which one participants tend to pick? Out of every 10 American workers, 7 consider a smartphone their primary learning channel, and 63% consider themselves dual-channel learners, strategically switching off between mobile devices and PCs.2

Based on the volume of requests for proposals from plan sponsors who still ask about onsite meetings, it seems that employees and employers may be a little out of sync on the topic of virtual learning. But plan sponsors who go digital have nothing to fear:

- With online registration and attendance logging, it’s still possible to determine who’s getting the plan information they need.

- Live webinars allow for real-time questions and answers.

- Digital sessions can connect seamlessly and instantaneously to an appropriate action—whether it’s enrolling, saving more, or exploring a new investment option.

5 Regular online learners are one step closer to financial wellness

With fewer than 20% of 401(k) participants confident in their ability to make financial decisions,3 financial wellness benefits have become pretty hot industrywide, and online involvement is the key to making them work.

Collectively, the calculators, videos, articles, and game-inspired learning modules can help create better budgeters, investors, and planners. Today’s planning hubs can create personalized and compelling experiences; however, a workforce’s financial IQ is most likely to be raised by plans that cultivate online education and engagement.

6 There’s an exciting spectrum of learning opportunities available

In our opinion, the best educational strategy a plan sponsor can take is to stay flexible. Relevant, high-quality content will always be important, but reaching out to all participants through the media they prefer can also make a big difference in the outcomes they achieve.

Among the educational options you get to choose from today are:

- Multimedia learning—Applies advanced design and user-experience techniques to improve participants’ knowledge and skills

- Live online learning—Adds anytime, anywhere flexibility to sessions led by the presenter or financial professional

- On-site financial professional-led learning—Dovetails with consultative and planning services offered by your financial professional

- On-site presenter-led learning—Involves face-to-face sessions led by an experienced (and often licensed) financial educator, and is mostly coordinated by the plan recordkeeper

One size of education won’t fit all, but today’s options can make an avid and successful learner out of virtually every employee.

As work and home merge, 401(k) online engagement helps retirement plans keep pace

With remote workforces and work-from-home policies growing, plan sponsors need to be creative to engage their employees. Whether the goal is increasing retirement readiness or alleviating financial stress, online learning and engagement strategies can play a key role. Partner with your financial professional and plan recordkeeper to design an approach that works for you and your participants.

1 John Hancock internal data, as of 12/31/18. 2 “Modern Learning: 6 Reasons Why Learning Has Changed Forever,” elearningindustry.com, 6/21/16. 3 John Hancock’s sixth annual financial stress survey, John Hancock and Greenwald & Associates, 2019. A survey of more than 3,500 workers to learn more about individual stress levels, their causes and effects, and strategies for relief.

Important disclosures

Important disclosures

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

MGTS-P41990-GE 4/20 MGR0408201135812